Financial planning may help you reduce the tax due on the sale of your business

What you need to know about your defined benefit pension

The 3 common ways a pension could be split during a divorce

2 crucial steps you may take to prepare for financial shocks

10 LIFE MILESTONES THAT FINANCIAL ADVICE COULD HELP YOU NAVIGATE

Financial advice can add value to your life. It could help you grow your wealth and improve your overall wellbeing.

A long-term study from the International Longevity Center suggests working with a financial planner could help you get more out of your assets.

The study assessed how the assets of people that received professional financial advice between 2001 and 2007 changed by 2012/14. It discovered, on average, those who took advice saw a total wealth boost of more than £47,000, including a significant increase of £31,000 to pension wealth.

In fact, when compared to people that did not take advice, “non-affluent” people working with a financial adviser benefited from a 35% uplift in their wealth. For “affluent” individuals it was 24%.

£47,000

The average person who took financial advice benefited from a wealth boost of

35%

Compared to those who didn’t take advice, advised “non-affluent” individuals saw an uplift in their wealth of

The research indicates financial planning could boost your wealth over the medium and long term.

What’s more, a separate survey suggests the nonfinancial benefits of seeking advice could be just as valuable. A report in Professional Adviser states 54% of people seek financial advice for their peace of mind.

Having a bespoke financial plan that’s aligned with your goals and considers your concerns could help you feel more confident about your finances.

FINANCIAL ADVICE COULD HELP YOU DURING KEY MILESTONES

While financial advice may be valuable throughout your life, it might be particularly useful during milestone events where the decisions you make could affect your long-term finances.

Specialist, tailored advice could help you navigate changes to your finances or life in a way that reflects your goals.

Among the scenarios where financial advice could be beneficial are when:

- You’ve secured a promotion or a new job – page 4

- You want to prepare for unexpected shocks – page 6

- You’re getting married or expecting a child– page 9

- You’re going through a divorce – page 14

- You’ve received a lump sum – page 17

- You’re preparing to sell your business – page 20

- You want to understand how to secure the retirement you want – page 22

- You’re nearing your retirement date – page 24

- You want to lend financial support to loved ones – page 27

- You’re thinking about your estate plan – page 30

Read on to find out what financial challenges you could face in these scenarios, and how effective financial planning could help.

1. YOU’VE SECURED A PROMOTION OR A NEW JOB

Changes to your regular income could present the perfect opportunity to review your finances and get the most out of your money now and in the future.

As your income increases, whether through promotion or a new job, reviewing your finances could help ensure your plan continues to reflect your financial circumstances.

This is a step you may take several times during your working life. In fact, according to Zippia, the average Brit will have 12 jobs during their lifetime and, hopefully, there will be pay rises and promotions along the way too.

Zippia also found the average salary increase when changing jobs is 14.8%. So, as your career progresses, your salary could rise sharply.

When reviewing your finances, it may be a good idea to consider both the short and long term.

REVIEWING YOUR SHORT-TERM BUDGET

When your income increases, you may see fewer reasons to budget. After all, if you have more than enough to cover essential expenses, you may not need to watch your outgoings as closely.

However, it can be easy for your everyday expenses to rise without you being aware – this is commonly called “lifestyle creep”.

Perhaps you’re more likely to treat yourself when you’re shopping? Or you’re more generous when you’re buying gifts for loved ones?

Your expenses increasing isn’t necessarily a bad thing. Improving your lifestyle and having more financial freedom are common reasons to seek promotions or switch jobs. Yet, it’s important to evaluate if these expenses are making you happy or contributing to other goals.

Research from Aegon found only 1 in 5 people are very aware of the day-to-day experiences that give them joy and purpose in life.

Being more conscious of how you use your money could mean you make choices that reflect what brings you happiness.

That doesn’t mean you have to reduce discretionary spending – splurging on a meal with family or friends could make you happy. It’s about deciding how to use your money to create the life you want.

As well as reflecting on what’s important to you now, reviewing your budget could help you take steps to secure a future you’re looking forward to.

Could workplace benefits help your money go further?

When you’re weighing up how to make your money go further, it’s worth reviewing if your workplace offers any benefits that could help.

For example, salary sacrifice schemes could provide a way to reduce your tax bill now. Or your employer may match your pension contributions and, if so, increasing the amount you’re paying into your pension could deliver significant long-term benefits.

Checking your employee handbook or speaking to your workplace’s human resources department may identify potential benefits that are useful.

Remember, an attractive perk isn’t automatically right for you. You should consider if it fits into your wider plan before you proceed.

SETTING YOUR LONG-TERM GOALS

The decisions you make about your money now could have a long-lasting effect. While you may focus on the present, setting long-term goals could secure the future you want.

Whether you want to buy property in the next five years or are looking forward to a retirement in several decades where you travel the world, planning is essential.

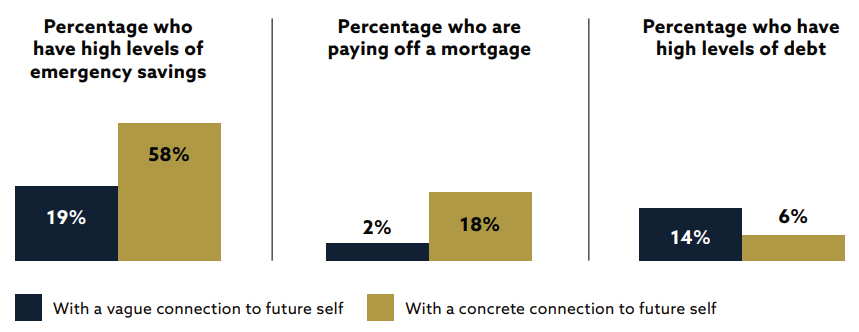

Yet, the Aegon report found only 18% of people have a plan to achieve long-term goals, and this affects their financial decisions.

People that have a firm picture of their desired future are more likely to build emergency savings, manage debt more effectively, and be homeowners.

Source: Aegon

Creating a financial plan could mean you’re more resilient to unexpected shocks and are more likely to reach your goals.

As your income increases, there may be steps you can take towards your aspirations. Depending on your goals, this may include:

- Increasing your pension contributions so you could retire sooner or have greater financial freedom when you give up work

- Boosting your investment portfolio to grow your wealth over the long term, which you may want to use to retire, leave as an inheritance, or support other goals

- Setting money aside that you could use to lend a helping hand to your children in the future, such as paying for university or a deposit to get on the property ladder

- Overpaying your mortgage so you can become mortgage-free sooner and have more disposable income later.

Reviewing your finances when your salary increases provides an opportunity to understand how you could use the additional income as a stepping stone to larger goals.

Financial planning may help you balance short-term spending with long-term goals when your income changes. It could mean you’re able to get more out of your money and identify how to use it to boost your overall wellbeing.

2. YOU WANT TO PREPARE FOR UNEXPECTED SHOCKS

The unexpected happens. While you can’t prevent unforeseen circumstances, you may take steps to improve your financial resilience so you’re in a better position to weather shocks.

A financial shock is an unexpected event that might harm your finances. For example, it could be an accident that means you need to take time off work, or if you have to replace your home’s roof due to a leak.

While a financial shock can occur at any point in your life, it’s common to start thinking about the effect it could have when your circumstances change.

Common triggers for considering your financial resilience include:

- Taking out a mortgage

- Getting married

- Having children

- Switching jobs.

A financial shock may have an immediate effect on your finances. In the case of needing to take time off work, your income may stop. It could mean you face pressure meeting your essential outgoings.

Additionally, it could affect your long-term financial security. You might dip into savings to cover costs or stop contributing to your pension.

DO YOU THINK “IT’LL NEVER HAPPEN TO ME”?

- Losing your job can place significant pressure on your short-term finances. It may also affect long-term plans. Economic uncertainty means 3 in 10 employers are likely to make redundancies in 2023 and 2024, according to Acas research.

- Thinking about serious illness can be difficult. As well as the effect it has on your health and wellbeing, you may need to take time away from work to recover. Government figures show 8% of employees have experienced a long-term sickness absence lasting four weeks or more.

It’s often factors outside of your control that cause a financial shock. While you can’t prevent them from happening, you can change how prepared you are and how you respond.

2 CRUCIAL STEPS YOU MAY TAKE TO PREPARE FOR FINANCIAL SHOCKS

1 Create an emergency fund

As the name suggests, an emergency fund is a pot of money you can draw on when you face unexpected expenses. From repairing the boiler to covering your mortgage payments if you’re not working, an emergency fund could provide a valuable safety net.

Yet, despite its importance, research suggests it’s something many people don’t have. According to HSBC, 1 in 6 UK adults have no savings. This could place them in a vulnerable position financially if they experience a shock.

How much you should hold in your emergency fund will depend on your budget and the other steps you’ve taken to boost your financial resilience. A general rule is to have enough money to cover between three and six months of essential outgoings.

You want your emergency fund to be readily accessible when you need it, so a cash account often makes sense. However, that doesn’t mean you shouldn’t look for ways to get the most out of your money.

Interest rates are higher than they have been in more than a decade. Shopping around could mean you find an account that’s right for you and offers a higher interest rate so your savings may grow at a faster pace.

2. Assess if financial protection could be right for you

- If you needed to stop work due to an illness or an accident, income protection could provide you with a regular income. It would continue to pay out until you return to work, retire, or the term ends.

- Being diagnosed with an illness could affect both short- and long-term finances. Critical illness cover would pay out a lump sum if you were diagnosed with an illness that’s covered under your policy terms.

- Term life insurance would pay out a lump sum to your loved ones if you passed away during the term. It could be useful if your family relies on your income by providing them with financial security. You could also choose whole-of-life insurance, which would pay out on death at any time.

An Aegon report suggests almost 7 in 10 people don’t have life insurance, critical cover, or income protection to fall back on.

You would need to pay regular premiums to maintain your cover. The cost of premiums will depend on a range of factors, from the potential payout to your age.

While the cost of premiums is something you need to consider, you should also weigh up how comprehensive the protection is. Sometimes, spending more could mean you have greater security.

5 of the Biggest Financial Protection Myths Busted

“Financial protection doesn’t pay out”

It’s a common misconception that if you make a financial protection claim, it won’t pay out. However, statistics from the Association of British Insurers shows financial protection policies paid out a total of £6.85 billion in 2022. What’s more, insurers accepted 98% of claims.

“I wouldn’t benefit from financial protection”

While no one wants to have to make a financial protection claim, the unexpected does happen. For example, the NHS states 1 in 2 people will develop some form of cancer during their lifetime. Taking out appropriate financial protection could help you prepare for the unforeseen.

“Financial protection is too expensive”

The cost of financial protection varies, but it may be cheaper than you think. A range of factors, from your age and health to the level of cover you want, will affect your premiums. The cost may differ between providers too, so shopping around could be worthwhile.

“I already have enough protection through work”

Your employer may provide you with some protection. For example, they may offer an enhanced sick pay policy that would mean you receive an income if you were too ill to work. Workplace perks may affect what financial protection is right for you, but there might still be gaps – how long would you receive sick pay for?

“I have a pre-existing condition so I can’t take out financial protection”

Pre-existing conditions could mean it’s more difficult to take out financial protection, but there are specialist providers. You may also take out protection that excludes pre-existing conditions.

As financial planners, we could help you identify potential gaps and risks in

your finances. We could also explain what steps you may take to improve your

resilience and provide peace of mind.

3. You're Getting Married or Expecting a child

Whether you’re planning a wedding or preparing to become a parent, changes to your family can be an exciting time. Yet, they can also raise new financial questions and challenges.

Taking a new step in your relationship could lead to important money conversations and decisions.

Whether you’re moving in with your partner, planning a wedding, or preparing for another relationship milestone, it could affect your finances too.

While important, discussions about money can be fraught. In fact, according to a survey from Royal London, money is the number one issue that couples argue about.

62%

of people say they have argued about money

24%

of people in a relationship consider their partner to be irresponsible with money

33%

of couples say they’re financially incompatible with their partner

1 in 3 people say they keep financial secrets from their partner, including hidings savings and debt

Source: Royal London

You and your partner may have very different attitudes to money or goals that can be difficult to navigate. It can be frustrating and lead to issues within your relationship. So, finding a way to bring your finances together could be essential for the health of your relationship.

Working with a financial planner as a couple could help you both get on the same page when it comes to finances.

Having a frank conversation about your assets, income, and what you want to achieve over the long term could help you work towards shared goals effectively. It may mean your dream of retiring early or setting up your own business is more likely to become a reality.

5 useful tips for talking about money with your partner

- Make money part of ongoing conversations rather than a topic you discuss every now and again. This can help you both feel included in financial decisions. Transparency about your finances could prevent potential issues escalating into arguments.

- It’s not just the figures that are important – so is understanding each other’s values. So, when you’re reviewing money, as well as looking at your income and outgoings, consider what your shared financial priorities are.

- Don’t be afraid to tackle the “big” money topics. Agreeing on areas like your household budget is essential, but talking about how much you need to save for retirement or what would happen if one of you faced a serious illness, are vital for long-term plans.

- Keep your finances organised. Knowing where all your paperwork is and what each asset is earmarked for can make your finances clearer and minimise potential conflicts.

- Work with a financial planner when you’re discussing money. This could be useful for two key reasons. First, your financial reviews provide the perfect opportunity to sit and talk about your finances and goals. Second, having a professional on hand to explain areas like tax efficiency or investment risk could prevent miscommunication.

Planning as a couple could your tax bill

Working towards goals together isn’t the only benefit of creating a financial plan with your partner. It could also present an opportunity to use allowances more effectively to cut your combined tax bill.

Many tax allowances are for individuals. Both you and your partner could use tax breaks, such as the:

- ISA annual allowance

- Pension Annual Allowance

- Annual exemption for Capital Gains Tax (CGT)

- Dividend Allowance.

For example, CGT is a tax you pay on the profit of certain assets when you dispose of them. For 2023/24, the annual exemption means you can make a profit of up to £6,000 before CGT is due – the allowance will fall to £3,000 in 2024/25.

As you can pass on assets to your spouse or civil partner without being liable for CGT, careful planning could allow you to make use of both of your annual exemptions. It’s a step that could reduce your overall tax liability as a couple.

The Marriage Allowance could cut your Income Tax bill

If you’re married or in a civil partnership, you could use the Marriage Allowance to reduce how much Income Tax you pay.

The Personal Allowance is the amount you can earn before Income Tax is due. In 2023/24, it is £12,570. If you or your partner doesn’t exceed this threshold, the lower earner may be able to pass on some of the unused allowance.

You can pass on £1,260 of your Personal Allowance, which could reduce your combined Income Tax bill by up to £252 a year.

To benefit from the Marriage Allowance, the person with the higher income must be a basic-rate taxpayer.

Getting your finances in order could provide peace of mind as a new parent

Preparing to welcome a child is an exciting time, but it’s also a milestone that could substantially change your finances.

It’s likely that a new baby will alter your day-today outgoings and could affect your income too. So, reviewing your budget now could mean you feel comfortable with your finances.

Changes to your household budget may affect long-term plans as well. For instance, could childcare costs mean you have less to contribute to your pension or investments in the future?

A financial review may help you stay on track for other life goals you have.

According to research, the cost of raising a child from birth to 18 in the UK is more than £200,000 – or £938 a month.

Source: LV=

Starting a nest egg could provide your child with more more opportunities

If you’re welcoming a new child, your thoughts might be focused on sleepless nights or the milestones that are to come. But thinking further ahead and creating a nest egg could be valuable.

You might have thought about your child’s education, and perhaps plan to send them to private school.

According to the Institute for Fiscal Studies, the average private school fee across the UK in 2022/23 was £15,200. Over 13 years of compulsory education, that adds up to a huge £197,600. Once you add in extracurricular activities or boarding options, the final figure could be much higher.

- Learn to drive and buy their first car

- Attend university

- Get on the property ladder

- Travel the world.

There are many different options when you want to create a nest egg, including a Junior ISA (JISA).

Like their adult counterparts, a JISA is a taxefficient way to save or invest. In 2023/24, the JISA allowance is £9,000.

One thing to keep in mind is that you usually cannot make withdrawals from a JISA before the child is 18. Once your child turns 18, they will have access to the savings and can use the money how they wish.

When your family is growing, creating or updating your financial plan to reflect new longterm goals or concerns you may have could ensure your financial decisions continue to reflect your changing needs.

Life insurance v family income benefit

Expecting a child is a common trigger for considering financial protection, and it could provide financial security if the worst should happen.

Both life insurance and family income benefit would pay out if you passed away during the term. However, how they do so is different, and it’s worth weighing up which might be right for your family.

Life insurance would pay out a lump sum, which your family could use how they like. For example, they may pay outstanding mortgage debt, school fees, or cover everyday living expenses.

In contrast, family income benefit would pay a regular income for a set period.

While family income benefit is less flexible, it could be a valuable option if your family would be overwhelmed or struggle to manage a lump sum payment. A regular income might provide greater peace of mind for some.

You can read more about the benefits of financial protection, and how it could create security on page 7.

Working with a financial planner could provide you and your partner with an opportunity to discuss topics that may be difficult or complex. By creating a financial

plan together, you can work towards shared goals and other milestones in the future.

4. You're Going through a Divorce

When you’re going through a divorce, assets and a long-term plan may be the last thing on your mind. Yet, the outcome of divorce proceedings could have a long-lasting effect on your life.

Going through a divorce may be emotional, and you could have a lot of decisions to make. This can mean that when separating couples are deciding how to split assets, some divorcees are mistakenly omitting key areas.

Ideally, a divorce settlement should fairly divide wealth. Yet, figures suggest that many people are overlooking some of their largest assets.

Research from Which? suggests 71% of divorcing couples don’t include pensions in their financial settlement.

It’s easy to see why divorcees often overlook pensions. They’re intangible and you may not be able to access them for decades. Compared to other assets, like property or savings, pensions could fall to the wayside when you’re negotiating.

However, failing to consider pensions could mean you miss out on vital savings and financial security later in life.

There may be other assets you forget too. Perhaps there are Premium Bonds or investments you’ve given little thought to for years, for example.

A financial divorce settlement is legally binding, so it’s essential you consider all areas from the start. To achieve a fair settlement for both you and your ex-partner, understanding all your assets and their value is often a good first step.

Financial planning could be useful here. We can work with divorcing couples to accurately calculate the value of their estate and understand how they may split assets fairly. Knowing a professional has assessed the assets could mean you feel more confident when you’re discussing options.

1. Pension offsetting

With pension offsetting, both you and your partner would retain the pension benefits you’ve built up. If one partner has a smaller pension, they may receive a larger portion of other assets.

This may be a good choice if you want a clean break and to keep your pension intact.

However, you should consider the long-term consequences. Not claiming any of your expartner’s pension in favour of a larger proportion of your home may seem sensible, but could it mean you suffer a shortfall later in life?

2. Pension sharing

If you’d like to split pensions in divorce while still having a clean break, a Pension Sharing Order may provide a solution.

A Pension Sharing Order would award a portion of one party’s pension to the other. The person that is awarded the pension benefits must transfer the money to another pension scheme. As a result, both you and your ex-partner would have full control over your own pensions.

3. Pension earmarking

When using pension earmarking, the person with the larger pension would agree to give their ex-spouse a portion of their pension when they start to take an income from it.

Usually, you can receive the money as an income throughout retirement or as a lump sum. However, in Scotland, it must be received as a lump sum.

While pension earmarking means you don’t have to make any changes to your retirement savings now, it can create complexities in the future. It means your finances could remain linked to your partner and their decisions could also affect you.

Pension earmarking may also be known as an “attachment order”.

Reassessing your priorities and goals could helpyou get back on track

Taking stock of your circumstances after a divorce could be useful.

Your financial situation may be very different following a relationship breakdown. From your household income falling to expenses increasing, creating a new budget that suits your new life may help get your finances in order.

As well as the day to day, you may also want to consider long-term finances. The divorce settlement may affect your retirement savings, or you may now be paying a mortgage for longer than expected.

What’s more, your goals may have changed drastically too.

Previously, you may have set goals with your ex-partner. Reassessing what your priorities are after a divorce can help you focus on what’s important to you – what do you want your future to look like?

Financial planning could help you bring together your new financial circumstances and goals to build a plan that’s right for you. Being proactive may mean you’re more likely to create the new life you want.

In addition, you may also need to update your estate plan. For instance, is your ex-partner:

- A beneficiary in your will?

- Named in your pension expression of wishes?

- A beneficiary of your life insurance?

A complete financial review after you’ve divorced could help you build the life you want and provide reassurance during a time of change.

Whether you’re going through a divorce now or want to assess your finances after a relationship has broken down, as financial planners we can offer you support. A tailored plan could help you feel more confident about the future.

5. You've Received a Lump Sum

Receiving a wealth boost could be life-changing and provide you with far more freedom. Yet, it can be overwhelming too, and you may be unsure how to make the most of the lump sum you’ve received.

There are many reasons why you may receive a significant lump sum during your life, from inheritance to redundancy. You could even win big on the lottery or Premium Bonds. While it’s a milestone that could change your life, it’s also one that can be difficult to navigate.

Your wealth changing suddenly could mean you now have more options than you previously thought possible. It may also mean you need to consider new financial issues, like whether the interest your savings earn is liable for tax or what the maximum amount you can add to your pension is.

Emotions may change how you feel about the money and related decisions too. This is often the case if you inherit wealth, as you may feel pressure to use the money in a certain way or a degree of guilt about receiving it at all.

A large wealth transfer is something many people will experience in their lifetime.

According to Money Age, 60% of millennials and Generation Z are expecting to receive an inheritance from their parents or other family members – 19% expect to receive more than £600,000.

Yet, there’s no “right” way to use the money.

You should consider what could improve your wellbeing now and in the future.

As your aspirations are at the centre of a financial plan, working with a financial planner could result in a strategy that leads to you getting more out of the money.

5. Practical steps that could help you make the most of your lump sum

1. UNDERSTAND HOW YOU WILL RECEIVE THE LUMP SUM

If you haven’t already received the lump sum, make sure you understand what needs to happen and the expected time frame.

While it can be tempting to start making plans straight away, depending on your circumstances, it could take far longer than you anticipate. For example, if you’re a beneficiary in a will, the probate process could take months, particularly if the estate or the benefactor’s wishes are complex.

In some cases, you may also need to consider if the assets you receive could be liable for tax.

2. GIVE YOURSELF SOME TIME

You don’t need to make big decisions about how to use the money immediately. In fact, giving yourself some time could be valuable.

Whether you’ve unexpectedly won a windfall or a loved one has left you an inheritance, you may experience a lot of different emotions. Taking a step back for a while may let you process the news and help put you in a positive frame of mind for making decisions.

3. REVIEW YOUR FINANCIAL RESILIENCE

If you want the money to create long-term financial security, reviewing your financial resilience is often a good place to start.

What financial safety net do you already have in place? Boosting your emergency fund could create a sense of security and mean you have assets to fall back on if the unexpected happens.

4. SET OUT YOUR GOALS

Once you’ve had time to think about what’s important to you, try setting some clear goals.

Maybe you want to retire in your 50s so you can spend more time with family and indulge in other passions? Or perhaps you want to set up your own business?

By outlining your priorities, you could create a blueprint for how you’ll use the lump sum to reach your goals.

5. ARRANGE A MEETING WITH A FINANCIAL PLANNER

A financial planner can help you bring together your goals and money, including after you’ve received a boost to your finances. A bespoke plan could provide a way for you to get more out of your money in a way that reflects your aspirations.

In addition, a financial plan may help you consider areas like tax liability and how you’d like to pass on wealth to your loved ones.

The Financial Services Compensation Scheme protects money in your bank account

You might feel nervous about having a lump sum sitting in your bank account while you decide how

to use it. The Financial Services Compensation Scheme (FSCS) could offer some reassurance.

The FSCS could provide compensation if a financial firm failed.

Usually, the FSCS covers up to £85,000 for each person per bank, building society, or credit union.

This rises to £1 million for six months when you deposit qualifying temporary high balances,including inheritances.

If your lump sum exceeds these thresholds, you can spread it across several accounts.

Keep in mind the FSCS treats financial institutions that share a banking licence as one bank. For example, if you held £85,000 in a HSBC account and £85,000 in a First Direct account, the FSCS would only cover half of your savings as the institutions share a licence.

The Bank of England provides a list of banking brands that are protected by the FSCS.

Financial planning could help you understand how to use the wealth you’ve

received to take a step closer to your goals. If you feel overwhelmed by the

financial decisions you need to make, we could also provide advice that leads to

you feeling more comfortable and confident.

6. You're Preparing to sell your Business

Selling your business is an exciting step and you may be looking forward to the next chapter of your life. Yet, there are financial considerations too, from how much you should sell your business for to understanding the tax bill you may need to pay.

If you’re preparing to sell your business, one of the key questions will be how much it will sell for.

Naturally, you want to sell it for the highest price possible. You may have spent decades building the business up and you could have complicated emotions about moving on.

While holding out for a “better” offer might seem sensible if you feel like a prospective buyer is undervaluing your business, it could mean you miss out in other ways.

You’ve decided to sell your business for a reason, but how would delaying the sale affect your future plans? It may mean you’re putting off opportunities or experiences you’re looking forward to.

As with many areas of finance, putting your longterm goals at the centre of your decisions could help you understand what’s right for you.

Understanding how much you need to sell the business for to secure the lifestyle you want to enjoy may put potential offers into perspective. If an offer you feel is too low would allow you to be financially comfortable and reach other goals, would accepting it improve your wellbeing overall?

Understanding what is “enough” to reach your goals could help put you in a stronger position to evaluate offers and confidently accept or reject them. If you’re unsure how much you need to secure your future, financial planning could provide an answer. We’ll take the time to understand how you could use the sale of your business to create long-term security and financial freedom to pursue your new goals.

FINANCIAL PLANNING MAY HELP YOU REDUCE THE TAX DUE ON THE SALE OF YOUR BUSINESS

When you sell a business, the profits you make could be liable for Capital Gains Tax (CGT). Fortunately, Business Asset Disposal Relief (BADR) could reduce the rate you pay.

For the 2023/24 tax year, you can make profits of up to £6,000 before CGT is due thanks to the annual exemption. You should note that the annual exemption will halve in 2024/25 to £3,000.

Profits that exceed this threshold could be liable for CGT.

The rate you pay will depend on your other taxable income. The standard rate of CGT is 10% (18% on residential property), and the higher CGT rate is 20% (28% on residential property). So, when selling your business, you could face a significant tax bill.

However, BADR could potentially halve the tax rate you pay, as qualifying business assets have a CGT rate of 10%.

To use BADR, you must be a sole trader or a business partner of the firm and have owned the business for at least two years.

You could also use BADR when selling shares or securities. You must be an employee or office holder of the company for at least two years to do so.

There is a BADR lifetime limit of £1 million. If you exceed this, the regular rate of CGT will apply.

To claim BADR, you’ll need to complete a self-assessment tax return. If you have any questions about taxes when selling a business, please contact us.

ONGOING FINANCIAL REVIEWS MAY HELP YOU STAY ON TRACK AFTER SELLING A BUSINESS

As well as providing financial advice when you’re preparing to sell your business, we could also offer ongoing financial support.

Selling your business could mean huge changes in your life, finances, and long-term plans. Whether you want to relax for a while or you’re eager to start another business, financial planning could provide you with peace of mind and financial security.

Regular reviews that focus on your aspirations may ensure you remain on track. A long-term financial plan could help you get more out of the next chapter of your life and ease worries about your financial circumstances.

Financial planning can provide essential support when you’re selling your business. By better understanding your finances now and in the long term, you could be in a better position to make decisions that are right for you.

7. You want to understand how to secure the retirement you want

Securing the retirement you want often requires a proactive approach to saving and understanding your goals.

Pension auto-enrolment means more workers than ever before are saving for retirement. Yet, the minimum contribution level could lead to an income that falls short of expectations.

A study from Scottish Widows suggests a third of Brits could be facing hardship in retirement. A further 18% are on track for an income that will cover a “minimum lifestyle”.

Less than half of employees are saving enough to look forward to an income that will provide financial security and flexibility.

So, what are you contributing to your pension, and how will it add up over your working life?

If you have a defined contribution pension, there are usually four ways your pension will grow:

- Your contributions: Under auto-enrolment, you will be contributing a minimum of 5% of your pensionable earnings (including tax relief) to your retirement savings. You can choose to increase the amount, either through regular or one-off contributions.

- Employer contributions: Your employer must contribute a minimum of 3% of your pensionable earnings. Some employers may offer higher contribution levels as a workplace benefit.

- Tax relief: To encourage you to save for retirement, the government adds some of the money you would have paid in tax to your pension. Make sure you’re claiming your full entitlement – if you are a higher- or additional-rate taxpayer, you’ll need to complete a self-assessment tax return.

- Investment returns: Usually, your pension savings will be invested. While returns cannot be guaranteed, over the long term, this could help your pension pot grow.

By understanding what’s going into your pension each month, you can start to calculate how much you could have when you retire.

While useful, these figures alone aren’t enough if you want to have confidence in the steps you’re taking.

SETTING OUT YOUR RETIREMENT DREAM PUTS YOUR SAVINGS INTO PERSPECTIVE

When calculating how much you need to save for retirement, there isn’t a single answer – it depends on the retirement lifestyle you want.

Even if retirement is years away, setting out your plans and potential income needs is valuable when you’re calculating if you’re on track. You may want to consider questions like:

- At what age would you like to retire?

- Do you plan to phase into retirement, or stop work completely on a set day?

- What would you like your days to look like when you retire?

- Are there any one-off expenses or experiences you’d like to make part of your retirement plan?

Your answers don’t have to be set in stone and you may want to make changes in the future, but they can provide your retirement plan with a clear direction. Your responses could provide a base figure for understanding if you’re saving “enough” or could face a shortfall.

We’ll bring together your savings and goals to create a tailored plan

When you approach us to understand if you’re on track for retirement, we’ll assess your assets and the steps you’re currently taking. We’ll also take the time to understand what your priorities are and what your dream retirement looks like.

By bringing together your current financial situation and your goals, we can create a plan that’s tailored to you. If there are potential shortfalls, we could offer advice on how to bridge them or where you could make compromises.

We can also offer advice on the most tax-efficient way to save for retirement, so your money goes further, and what level of investment risk is appropriate for you.

It’s never too soon to start retirement planning. Engaging with your pension and building a retirement plan earlier in your career provides you with more opportunities to put money away and make use of allowances that could boost your future income.

Whether your retirement date is drawing close or is decades away, a retirement plan may help you get more out of your money. It could help you take the steps you need to reach your goals once you stop working.

8. You are Nearing your Retirement date

Retirement may be a milestone you’ve been looking forward to for years. Yet, with decisions to make that could affect the rest of your life, aspects of retirement may feel overwhelming too.

If you’re nearing retirement, understanding your expected income, and how you’ll draw your later-life income, are essential steps. During your working life, you may have accrued several pensions.

How you could use them to create an income will depend on whether they’re defined benefit or defined contribution pensions.

WHAT YOU NEED TO KNOW ABOUT YOUR DEFINED BENEFIT PENSION

A defined benefit (DB) pension is sometimes referred to as a “final salary pension”. They are often generous and can provide financial security in retirement.

A DB pension will provide a regular income from your retirement date for the rest of your life. The income is often linked to the number of years you’ve been a member of the pension scheme and your average salary.

The income may be linked to inflation, which could help to preserve your spending power throughout retirement. In addition, it might come with auxiliary benefits, such as providing an income to your spouse if you passed away first.

As a DB pension will provide a guaranteed income, it could offer peace of mind and financial security once you stop working.

YOUR 3 MAIN OPTIONS WHEN ACCESSING YOUR DEFINED CONTRIBUTION PENSION

When you save into a DC pension, your money is added to a pot. Usually, you’ll benefit from tax relief and, if you’re employed, employer contributions too. This money is then typically invested with the aim of growing your pot over your working life.

As a result, when you reach retirement age, you’ll have a pot of money to create an income from.

You can access your DC pension from the age of 55, rising to 57 in 2028, and there are several options you’ll need to weigh up, each with pros and cons to consider.

While you may no longer be earning a salary, you could still be liable for Income Tax in retirement. If your income exceeds the Personal Allowance, which is £12,570 in 2023/24, the amount above the threshold would be taxable. So, you should be mindful of pension withdrawals and whether you could unexpectedly pay a higher rate of Income Tax.

As well as your pensions, you may also want to consider how you could use other assets to fund your retirement. Your savings, investments, or property could all be valuable when you’re creating a retirement plan. If you’d like help bringing together different income streams, please contact us.

1. Purchase an annuity

Purchasing an annuity is a way to generate a guaranteed income for the rest of your life if you have a DC pension.

You’d pay a provider a lump sum in return for a regular income. You may choose an annuity that would increase each year to maintain your spending power as the cost of living rises. You could also choose an annuity that would provide an income for your partner if you passed away.

Many factors will affect the income you receive from an annuity, including your age and health. A key factor in the amount you’d receive is the annuity rate.

Annuity rates can vary between providers, so shopping around if you decide to take out an annuity could boost your retirement income.

An annuity is less flexible than other options when you’re accessing a DC pension. However, a guaranteed income could be valuable and provide you with peace of mind.

2. Take a flexible income

By using flexi-access drawdown, you could take a flexible income from your pension.

With this option, you’d be in control of the income you receive from your pension. You can choose to take more or less to suit your needs. Usually, the money you don’t withdraw will remain invested and could deliver returns during your retirement.

While a flexible income could be useful if your income needs change throughout retirement, it’s an option that also comes with responsibility.

You’ll need to ensure your pension lasts for the rest of your life, and there is a risk that you could take too much too soon.

In addition, as your pension will often remain invested, it’s also important you understand what level of investment risk is appropriate for you. You should also be aware of how market volatility could affect the value of your pension.

Ongoing financial advice could help you manage taking a flexible income with longterm security in mind.

Withdraw lump sums

You could also choose to withdraw lump sums from your pension as and when you need to. You could even take all the money from your pension in a single withdrawal if you choose.

As with flexi-access drawdown, you’ll need to consider how accessing your money could affect your income in the future. If you’ll be taking large sums from your pension, you should keep the Income Tax thresholds in mind to avoid paying a higher rate than you expect.

Mix and match: You don’t have to choose one option

With a DC pension, you can mix and match the options to create an income that suits your needs.

For example, you could use a proportion of your retirement savings to purchase an annuity to create a base income and provide some certainty.

Using flexi-access drawdown, you could then supplement the income from an annuity when your income needs increase.

ONGOING FINANCIAL PLANNING COULD MITIGATE RETIREMENT CHALLENGES

Seeking advice from a financial planner could be valuable when you’re trying to understand your options when you access your pension. Yet, a financial plan goes far beyond your retirement date and ongoing advice may be beneficial.

Regular financial reviews can help you overcome some of the biggest challenges retirees face today.

As many are responsible for creating their own income in retirement, there’s a real risk that some retirees are withdrawing an unsustainable income. It could mean they run out of money during their lifetime.

The financial planning process could help you balance income needs with long-term financial stability.

Ongoing reviews and meetings may help you overcome other challenges too by considering different scenarios and taking steps to mitigate risks.

The Great British Retirement Survey found one of the biggest financial concerns is the rising cost of living – 3 in 5 said it was a “big worry”.

Retirees that didn’t consider the potential impact of a high inflation period could find their money no longer goes as far as it used to. For some, it may mean they’ve had to adjust their retirement lifestyle or future expectations.

The survey also found that 40% of retirees are worried about a stock market crisis and the effect it would have on their finances.

As a portion of your pension could remain invested throughout retirement, it’s essential you consider how volatility might affect your income.

With 65% of people agreeing their financial situation affects their mental health, retirement planning could ease your concerns by addressing potential risks.

A financial planner could help you navigate your retirement date and beyond. With someone to turn to for advice and support, you can focus on enjoying the retirement you’ve worked hard for.

9. You want to lend financial support to loved ones

Do you want to use your wealth to support the next generation of your family? A financial helping hand can have a hugely positive effect on the financial security of loved ones, but you also need to consider the implications for you.

Passing on wealth through gifting is becoming more common. You might want to provide financial support to help children or grandchildren improve their day-to-day finances or reach life milestones.

According to research from the Institute for Fiscal Studies, over a two-year period around 5% of adults will receive a substantial gift, and 2% will benefit from a substantial loan. Adults in their 20s and early 30s are more likely than other age groups to receive a gift.

While the median gift is around £2,000, the largest 10% of wealth transfers are more than £20,500.

The data suggests lifetime transfers are around a fifth of the annual flow of inheritances. So, for many people, gifting during their lifetime is an important part of transferring wealth.

Costly property prices are often a reason why families are discussing gifting.

Younger generations are struggling to save the deposit they need to buy a home. As property prices rise, the deposit first-time buyers need has increased at a much faster pace than wages.

In fact, estate agent Savills estimates 61% of first-time buyers will receive financial support from their family in 2023.

Many families are offering support to firsttime buyers in other ways too. For instance, they may provide a place for first-time buyers to live while they save a deposit or act as a guarantor on a mortgage.

There are plenty of other reasons you might want to lend a helping hand too, such as:

- Covering rising household expenses

- Paying for private school or university

- Supporting them through a financial shock

- Paying for a wedding

- Providing them with greater freedom.

If your loved ones are struggling financially, it’s natural to want to offer assistance. Yet, you need to consider your long-term inancial security too.

Calculating how gifting may affect your finances could provide peace of mind

While you may want to help loved ones, you might also worry about the long-term effects of giving away a lump sum – could it mean you run out of money or need to adjust your lifestyle later in life?

Reviewing your finances and understanding the implications of gifting first could allow you to feel confident when you make a wealth transfer.

As financial planners, we could help you assess the impact of gifting now, including how it might affect your lifestyle in the future. This understanding could deliver peace of mind or highlight potential risks so you can find a solution that doesn’t compromise your financial security.

If you do decide to gift, we can also offer advice on which assets to use to make the wealth transfer efficient.

Gifting and Inheritance Tax (IHT)

As well as supporting loved ones, gifting during your lifetime could be useful for another reason – it may reduce how much IHT your estate pays when you pass away.

By reducing the value of your estate, gifting could result in a lower IHT bill. However, simply handing over assets may not be suitable.

While some gifts are immediately outside of your estate for IHT purposes, others are “potentially exempt transfers” and may be included when calculating how much tax your estate is liable for.

Gifts that are immediately outside of your estate include:

- £3,000 during the 2023/24 tax year, known as the “annual exemption”

- Small gifts of up to £250 to individuals, as long as they have not benefited from other allowances

- £1,000 wedding gift, which rises to £5,000 and £2,500 for a child or grandchild respectively

- Gifts that are regular payments from your income and do not negatively affect your standard of living, such as paying the school fees of your grandchildren or paying the rent for a loved one.

Potentially exempt transfers may be included in IHT calculations for up to seven years if the value of your estate exceeds IHT thresholds, with the rate of tax decreasing over time. The table below shows how the tax rate changes.

| Years between gift and death | Rate of tax on the gift |

|---|---|

| 3 to 4 years | 32% |

| 4 to 5 years | 24% |

| 5 to 6 years | 16% |

| 6 to 7 years | 8% |

| 7 or more | 0% |

Remember that taper relief only applies to gifts in excess of the IHT nil-rate band. It follows that, if no tax is payable on the transfer because it does not exceed the nil-rate band (after cumulation), there can be no relief.

Taper relief does not reduce the value transferred; it reduces the tax payable as a consequence of that transfer.

If you want to gift to reduce a potential IHT bill, seeking financial advice could help you create a gifting strategy that suits your goals.

It’s also a good idea to keep a record of gifts, particularly if you intend to make regular payments as gifts as your estate may need to demonstrate that they were consistent.

To discover when your estate could be liable for IHT, read page 31.

When you want to lend a financial helping hand to your loved ones, financial planning can help you balance your goals and long-term financial security. We aim to help you feel confident in your finances, so, if you decide to gift, you understand the long-term effects.

10. You're Thinking about your Estate plan

An estate plan sets out what you want to happen to your assets during your lifetime and when you pass away. It can be complex and there are often many factors you need to consider to create an effective estate plan.

Creating an estate plan can be difficult. Not only could it be complex, but it may be emotionally challenging too.

Financial planning could add value as you devise your estate plan.

Understanding the value of your estate

One of the first tasks when creating an estate plan is to understand what your estate includes.

Your estate includes all of your assets. It may include property, savings, investments, and material possessions.

Pulling together information about all these different assets means you can start to understand how much your estate is worth.

This is important for two reasons. First, the value of assets or your entire estate may affect how you want to pass on wealth. Second, it could highlight if you need to consider whether your estate could be liable for Inheritance Tax (IHT).

As financial planners, we could help you get a better grasp of your estate and its value.

Should your family be part of your estate planning process?

There are benefits to including your family when you are creating an estate plan. It can provide an opportunity to understand their financial challenges and how you could offer support. It may also ensure they have realistic expectations about the assets you intend to pass on.

However, it’s not essential and there are a lot of reasons you may want to keep your estate plan to yourself. What’s important is that you’re comfortable with the decisions you make.

Calculating how the value of assets may change

Knowing the value of your assets now is important, but how will they change over the years?

During your lifetime the value of assets may change. Your pension or savings may decrease as you use them to create an income in retirement. Or the value of your home could rise.

Cashflow modelling as part of your estate plan could help you understand how different scenarios could affect your wealth.

For example, you could model how taking a higher income throughout retirement might affect the inheritance you leave. You may also model factors outside of your control, such different returns from investments.

While the results of cashflow modelling cannot be guaranteed, they can be instructive and help you understand your long-term financial security and assets. The outcomes could affect your estate plan.

Deciding who you want to benefit from your estate and how to pass on assets

Once you have a better understanding of your assets and how your wealth could change, it’s time to think about passing on assets. There are two key questions to answer – who do you want to benefit from your estate? And how do you want to pass on wealth?

Family members are likely to come to mind first when you think of passing on wealth. You may also want to consider charitable causes or organisations that are important to you as well.

There’s more than one way to pass on wealth as part of your estate plan. The three main

options are:

- Leaving an inheritance: Using a will to pass on assets after you pass away is the traditional way to transfer wealth. You can set out who you want to benefit from your estate, including naming specific assets you want to go to individuals.

- Gifting assets during your lifetime: As younger generations face financial challenges, it’s becoming more common to pass on wealth during your lifetime. While this option could mean you’re able to lend support when your family needs it most, you also need to consider how it could affect your long-term finances.

- Placing assets in a trust: You can set up a trust during your lifetime or create one as part of your will. A trust could provide you with greater control over how the assets are used. They can be a useful way to pass on wealth to children, ensure the assets stay within your family, and, in some cases, could reduce an IHT bill. Trusts can be complex, so seeking tailored financial and legal advice is often useful.

If your estate is worth more than £325,000, you may need to consider Inheritance Tax

- Leaving an inheritance: Using a will to pass on assets after you pass away is the traditional way to transfer wealth. You can set out who you want to benefit from your estate, including naming specific assets you want to go to individuals.

- Gifting assets during your lifetime: As younger generations face financial challenges, it’s becoming more common to pass on wealth during your lifetime. While this option could mean you’re able to lend support when your family needs it most, you also need to consider how it could affect your long-term finances.

- Placing assets in a trust: You can set up a trust during your lifetime or create one as part of your will. A trust could provide you with greater control over how the assets are used. They can be a useful way to pass on wealth to children, ensure the assets stay within your family, and, in some cases, could reduce an IHT bill. Trusts can be complex, so seeking tailored financial and legal advice is often useful.

When you pass away, if the value of all your assets exceeds certain thresholds, you may need to consider Inheritance Tax (IHT). There are usually steps you can take to reduce an IHT bill, but you’ll often need to be proactive.

In 2023/24, the nil-rate band is £325,000. If the value of your estate is below this threshold, your estate won’t be liable for IHT. If you will be leaving your main home to direct descendants, you may also be able to use the residence nil-rate band, which is £175,000 in 2023/24.

You can pass on unused allowances to your spouse or civil partner. As a result, if you’re planning as a couple, you could pass on up to £1 million before IHT is due.

The government has frozen both the nilrate band and residence nil-rate band until April 2028.

The portion of your estate that exceeds the thresholds could be liable for IHT at a rate of 40%. If you don’t want a potentially substantial proportion of your estate to go to HMRC, considering ways to mitigate IHT during your lifetime may be important.

As part of your estate plan, we can offer tailored advice about some of the steps you could take to reduce IHT, from gifting assets during your lifetime to leaving a charitable legacy. Please contact us to discuss IHT.

A will is an excellent way to ensure your wishes are carried out

Once you’ve set out who you’d like to benefit from your estate, you should consider writing a will to ensure your wishes are carried out.

You can choose to write your will yourself. However, working with a legal professional could help you avoid mistakes or ambiguous language.

As your circumstances and wishes may change, it is usually a good idea to review your will every five years and after major life events.

Intestacy Rules: How Would your Assets be distributed without a will?

If you don’t have a valid will in place, your estate would be distributed according to intestacy rules. This may not align with your wishes. The flowchart below shows what would happen to your assets if you pass away without a will.

The rules of Intestacy do not necessarily distribute assets in the most tax-efficient manner and do not always distribute assets in a way that an individual necessarily wants. This can be compounded where there have been second marriages and various children from previous relationships; or individuals simply cohabit.

To ensure an estate is distributed according to the wishes of the deceased and in a taxefficient manner, individuals should not rely on these rules but should seek advice to determine how best to distribute an estate in a tax efficient manner and create a suitable will.

Personal chattels are items of personal property such as clothes, jewellery and furniture.

Your spouse will only benefit if he or she survives you by 28 days. If your spouse does not survive for this period, then your estate will be distributed as if you had not been married.

You could use an estate plan to consider security in your later years too

While estate plans often focus on how you want your wealth to be passed on when you die, you may also want to consider your wishes for your later years.

Steps you take now could provide you with greater security and more freedom in the future. Here are two key steps you may want to take.

1. Register a lasting power of attorney

A Lasting Power of Attorney (LPA) gives someone you trust the ability to make decisions on your behalf if you don’t have the capacity to do so.

There are two different types of LPA:

- A health and welfare LPA would give an attorney the power to make decisions about things like medical treatment or moving into a care home.

- Property and financial affairs LPA would provide an attorney with the power to manage your bank account, pay bills or sell your home.

If you choose, you can name more than one attorney, and you may specify that they have to make all decisions together or if they can act separately.

For an LPA to be valid, you must register it with the Office for Public Guardian.

You can only put an LPA in place while you have the mental capacity to do so. While thinking about losing mental capacity is difficult, failing to register an LPA may place you and your loved ones in a challenging situation.

Without an LPA, your family is unlikely to be able to make decisions for you. They would need to apply to the Court of Protection to act on your behalf, which could be a lengthy and costly process. In the meantime, you could be left in a vulnerable position. There is also no guarantee that the Court of Protection would appoint the person you’d choose to act for you.

2. Set out a care plan

Again, care can be another difficult topic to contemplate. However, as most people will be responsible for at least a portion of their care costs if it’s required, making it part of your plan could be beneficial.

According to interactive investor, the average cost of a nursing home is more than £60,000 a year after a 10% increase in 2023 when compared to a year earlier

While you may not need care in the future, setting aside some of your assets to cover a potential bill could mean you have more choices. For instance, it may mean you’re able to choose a home that’s in your local area and close to family, or one that boasts facilities that would support your wellbeing.

Financial planning could help you build an estate plan that balances your needs now with your wishes for the future. From understanding how to pass on assets taxefficiently to creating peace of mind about your later years, we can work with you to build an estate plan that suits you.

Contact us to talk about your financial plan

Whether you’ve reached a life milestone or want to understand how financial planning could help you, we can answer your questions.

Please contact us to arrange a meeting to discuss your goals: