How do you grow your wealth when you’re investing? Choosing the “right” investments is just one of the ingredients needed for success. Indeed, your mindset and behaviours could have a much larger effect on the outcomes of your investments than you might think.

Your approach to investing could influence the decisions you make when you start building your portfolio, such as how much risk you take. It could also play a role in how you respond to market movements, which may have a knock-on effect on the long-term returns of your portfolio.

So, as well as considering which investments could help you reach your goals, you might also want to review your behaviours and the impact they could have.

Read on to learn more about seven behaviours that could help you reach your investment goals.

“Wealth isn’t primarily determined by investment performance, but by investor behaviour.”

– Nick Murray, author.

Please note: This guide is for general information only and does not constitute advice. This information is aimed at retail clients only.

A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The fund value may fluctuate and can go down, which would have an impact on the level of pension benefits available.

The value of your investment can go down as well as up and you may not get back the full amount you invested. Past performance is not a reliable indicator of future performance.

1. Recognise the opportunities that investing could offer

It might seem like an obvious place to start, but to potentially benefit from investing, you need to take the plunge and invest some of your money.

Investing could provide you with a chance to grow your wealth over the long term. Yet, research suggests that many people who could benefit from investing choose to hold their money in cash accounts.

In fact, an Aviva survey found that 37% of women and 24% of men don’t invest. Many reasons were listed for not investing, including the risk being too high.

While using a cash savings account might seem like the “safe” option, the value of your money may fall in real terms.

As the cost of goods and services rises, the spending power of the money held in your savings account will fall unless the interest you receive keeps pace with or exceeds the rate of inflation.

Let’s say you had £40,000 in a cash savings account in 2003. According to the Bank of England, between 2003 and 2023, inflation averaged 2.8% a year.

The investor of today does not profit from yesterday’s growth.” – Warren Buffett, investor.

To simply maintain their spending power, your savings would need to have grown to more than £70,000. So, if you didn’t receive around £30,000 in interest over 20 years, the value of your savings has fallen in real terms.

While investment returns cannot be guaranteed, investing provides an opportunity to grow your wealth in real terms.

That’s not to say that cash accounts don’t play a valuable role in many financial plans. They are a useful option if you may need to access the money quickly, such as an emergency fund, or you’re saving for short-term goals.

Setting out what you want to achieve with your wealth could help you assess if investing is right for you.

2. Invest with a purpose

Before you start selecting investments or funds, setting out your reasons for investing may be useful – what do you want to achieve through your investments?

Setting clear goals could help you make decisions that are right for you. Your purpose could affect areas like:

- How much investment risk is appropriate

- The time frame of your investment strategy.

For instance, if you want to invest to support your retirement in 30 years, you might decide that a pension is the right vehicle for your investments and, as the time frame is long, you may be in a position to take more risk. In contrast, if you want to build a nest egg for your child and plan to gift it to them in 10 years, you may wish to take a more cautious approach.

Having a clear reason also means you’re able to assess what “success” is for you. A purpose could help you understand what returns your portfolio would need to generate to improve your financial wellbeing and life.

In addition, tailoring your investment portfolio to your goals could boost your confidence during market volatility. Knowing that you made investment decisions based on your long-term aspirations could ease concerns you have and mean you feel more comfortable weathering periods of uncertainty or downturn.

3. Practise patience

For most, investing should be a marathon, not a sprint.

While the media can make it seem like investing is a way to get rich quick, the reality is that successful investing often involves a lot of patience and a long-term view.

Trying to time the market to deliver quick returns consistently is impossible. Numerous factors affect the markets and they don’t always react predictably. Even investment professionals with a dedicated team and resources can make inaccurate predictions.

Instead, creating a portfolio that’s appropriate for you and designed with the intention to deliver returns over many years may help you balance risk and achieve your goals.

As a general rule, it’s often recommended that you invest with a minimum five-year time frame. This could help smooth out the ups and downs of the market.

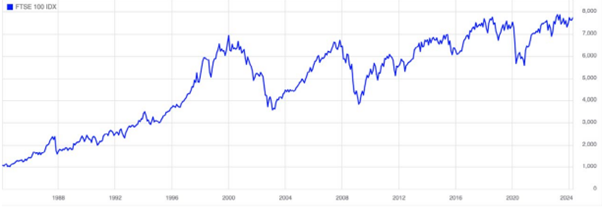

In 2024, the FTSE 100 – an index of the 100 largest companies on the London Stock Exchange – turned 40. Looking over its four-decade history could give an insight into how the ups and downs of the market might affect your portfolio.

The graph below shows the performance of the FTSE 100 between 1984 and 2024. There have been times when the index has fallen. Most recently, the Covid-19 pandemic led to a sharp drop. Yet, when you look at the overall trend, it’s been an upward one.

Source: London Stock Exchange

By taking a long-term view, dips in the market are less likely to have a negative effect on your goals, as there may be an opportunity for the value of your investments to recover and grow further.

If you want to grow your wealth, leaving your investments for a longer period means you could also benefit from the effects of compounding.

By reinvesting your returns, you may earn returns on both your original investment and on the previous returns. It could help your wealth to grow at a faster pace as time passes.

So, when you’re investing, practising patience could help curb impulses to try and time the market.

It’s waiting that helps you as an investor, and a lot of people just can’t stand to wait. If you didn’t get the deferred-gratification gene, you’ve got to work very hard to overcome that.” – Charlie Munger, investor. “

4. Stay calm during market volatility

As an investor, you will experience investments falling in value and market volatility at some point – it is part of investing. How you respond to the uncertainty could affect how successful you are.

If you see the value of your portfolio has fallen, it can be easy to worry and make an impulsive decision to sell your investments in response. You might be concerned that the value will fall further and think that by selling your assets now, you’re protecting yourself from additional losses.

Yet, by selling assets, you turn paper losses into actual losses.

Historically, markets have delivered returns over a long-term time frame. For many investors, holding assets, including during periods of volatility, makes sense for their financial plan.

History provides a crucial insight regarding market crises: they are inevitable, painful, and ultimately surmountable. – Shelby MC Davis, investor.

Indeed, by selling assets when you’re worried, you could miss out on some of the bestperforming days of the market.

According to figures from Schroders, if you’d invested £1,000 in January 1988 in the 100 largest UK companies and left the investment alone until June 2022, it might be worth more than £15,000 – an average annual return of around 8.3%.

However, if you’d missed just the 10 best days of the market, your return would fall to 6.1%. Miss the best 30 days and your returns could fall to 3.38%.

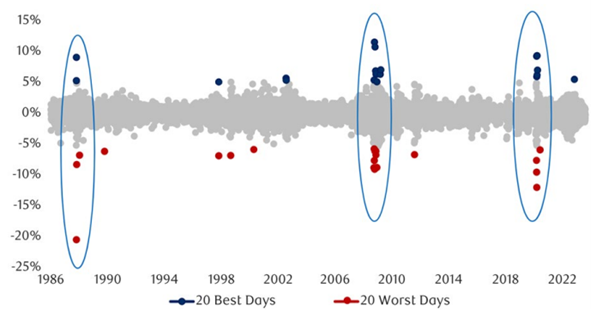

Interestingly, research from RBC also suggests the investment market’s best and worst days often happen close together. The S&P 500 is a stock market index that measures the performance of 500 companies in the US. The graph below shows the index’s best and worst days between 1986 and 2022.

Source: RBC

Making investment decisions based on fear or worry could mean you miss out on potential returns over the long term.

So, next time a negative emotion, like fear or anxiety, is making you question your investment strategy, taking a step back to evaluate the long-term performance and goals of your portfolio could help you become a more successful investor.

5. Be conscious of the effect of positive emotions

Investment decisions should be based on facts rather than your feelings, but they can have a significant effect on how you view certain investments or the market as a whole.

Fear isn’t the only emotion that could influence your investment decisions. Ones that seem positive, like excitement, could harm your portfolio’s performance too.

If you read a headline stating that the market is “soaring” or that a certain business is on track to post “massive” growth, you might be tempted to invest yourself. Indeed, the thrill of believing you’ve found an investment opportunity with excellent prospects could lead to you becoming overconfident. It might mean you take more risk than you normally would, or that you don’t look for more information.

Overconfidence is a type of behavioural bias that could lead to you making investment decisions that aren’t right for you.

Another example of positive emotions potentially affecting your investment decisions is herd mentality.

Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.” – Paul Samuelson, economist.

If you’re speaking to a group of friends who are enthusiastically talking about an investment they believe will deliver huge returns, you can get swept up in the excitement. It might mean you skip assessing if an investment is right for you or even overlook red flags.

Remember, your investment strategy should be tailored to you. So, while an investment opportunity might be right for other people, you should not automatically invest.

It can be difficult to be aware of when unconscious bias might be affecting your decision-making. Taking a step back could give you time to think objectively about your options and for emotions that may have been playing a role to subside.

6. Focus on creating a balanced portfolio not the next “big” opportunity

Every investor would love to find the company that will become the next Microsoft or Tesla to secure huge returns.

However, for every business that achieves a market capitalisation in the billions, there are many more that fail or deliver modest returns. So, rather than trying to discover and invest in a handful of companies, diversifying your investments may deliver more security and growth overall.

It may involve changing your investing mindset. Rather than thinking about uncovering the next big business, focusing on how to spread out your investments to achieve your aims might help you invest successfully.

It’s not just about the number of businesses you invest in either. For many investors, creating a balanced portfolio means investing in companies from a range of industries and geographical locations, as well as different assets.

Holding a range of investments could reduce the amount of volatility your portfolio experiences too. When one sector falls in value, a rise in another could provide balance.

Don’t look for the needle in the haystack, just buy the haystack!” -John Bogle, investor.

7. Work with a financial planner

A financial planner could offer you valuable support when you’re investing. As well as managing your investment portfolio on your behalf, they could also provide you with someone to turn to when you’re worried about performance or interested in a new opportunity.

Yet, a report in FTAdviserv indicates that many investors aren’t taking any financial advice. Research found less than a quarter of British investors work with a financial professional, and more than 4 in 10 have never used a financial adviser.

Having a professional to talk to about your options could help you reduce the effect of behavioural bias. Simply speaking to someone you trust could identify when your decisions are being influenced by emotions and help you make choices that are right for you.

There are other benefits of working with a financial planner too. We may be able to help you find ways to reduce your tax bill, help you understand how investments could support wider goals, and more.

If you’d like to arrange a meeting to talk about your investments, please contact us