What is compounding, and how does it work?

When a 1920s ad referred to compound interest as “the eighth wonder of the world”, the quote was left unattributed. But that did not stop it from becoming synonymous with the celebrated physicist, Albert Einstein.

The link was likely intended to lend credibility to a statement that at first glance seems bold. And yet, compounding could be key to the success of your long-term financial plans.

As Einstein did or did not say, “He who understands it, earns it; he who doesn’t, pays it.” Whoever did say this knew what they were talking about.

Compounding is a fundamental concept in finance and has a key role in investment projections, forecasting, and cash flow modelling.

Put simply, the term describes the process of receiving interest on interest, or growth on growth. When you save or invest money, it earns a yield in the form of interest or a dividend, which you might choose to receive as income. Equally, it can be reinvested.

Reinvesting means you are buying more units, and so increasing your investment, as well as the amount that you can receive a yield on in the future. The yield on your yield is compounding.

It’s the reason that your savings and investments snowball over time and can see exponential growth.

Consider professional guidance from Future Planning Swindon to maximize compounding benefits in your retirement and investment planning.”

Let’s look at a worked example using a regular savings account:

For argument’s sake, let’s say that your high street bank account offers interest at 5%. If you deposit £10,000 into your account, you’d expect to receive £500 interest after 12 months. Assuming you leave the initial sum and first year of interest in the account, in year two, you would receive a higher interest payment, even if the rate itself stays the same. This is because in your second year, you won’t receive interest solely on your initial £10,000 deposit. Interest is applied at 5% on your new savings amount of £10,500.In this example, 5% of £10,500 is £525. This is the effect of compound interest.

An extra £25 might not seem huge, but the snowballing effects of compound growth can make a significant difference over time.

It isn’t just savings accounts that benefit from compounding. Investments like your Stocks and Shares ISA and pensions take advantage of it too.

Maybe you receive dividends from your investments, alongside capital growth. Dividend reinvestment is a powerful compounding tool so you might consider lowering your income and reinvesting your returns instead.

Your pension fund, meanwhile, will be building over decades – plenty of time for compounding to take effect, with the possibility of exponential growth.

Over the long term, you might find that you reach the so-called compound investing “tipping point” – the moment at which your returns exceed what you have invested.

Just as compounding can work in your favour as it grows your saved and invested wealth, it can apply negatively too. Interest on debt also compounds and this can make it harder to repay the amount you owe.

A MAGIC PENNY

It might be easier to imagine compounding as like a magic penny that doubles in value every day.

Progress will be slow at first.

May 2025 You’ll need eight days before your penny is worth £1 but just 48 hours after that (on day 10) you’ll have £5.12.

As the value of your penny increases, so too do the jumps in value. This is because each increase includes the previous increase, and so on.

By day 20 your magic penny is worth more than £5,000 and before the month is out, you’ll have a massive £5.3 million saved.

Of course, no savings account or investment will provide returns like this. But, if someone offers you £1 million today or a magic penny for a month, it might be worth staying patient and adopting the longer-term approach.

3 benefits of compounding that could help boost your savings and investments

1. Compounding could help you reach your goals more quickly

Your long-term investments are aligned with your individual aims, attitude to risk, and time frames. Your ultimate goal might be retirement at 65, say. But the snowballing effects of compound growth could help you to reach your goals sooner.

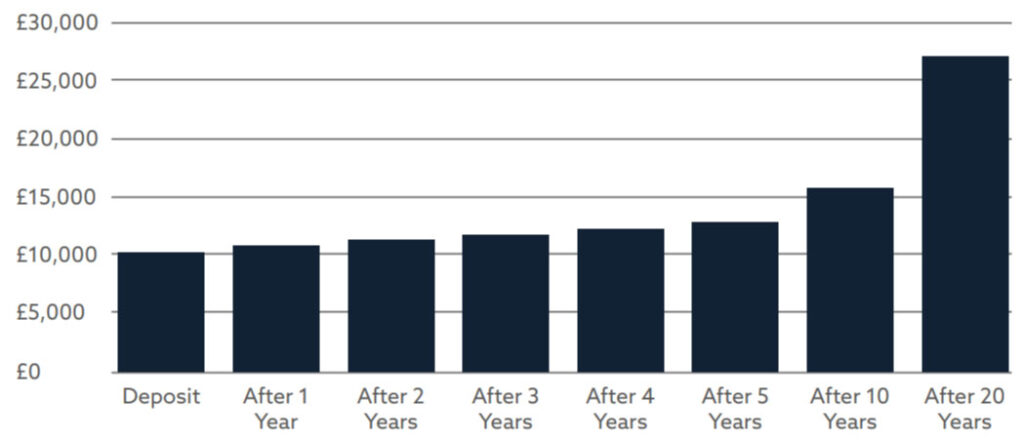

To return to our previous example, 5% interest on a £10,000 deposit or investment would provide an annualised return of £500. In this scenario, over a 20-year time frame, your initial £10,000 grows to £19,000.

Compound returns over the same period, though, would see your original deposit increase to £27,126.40, assuming returns remain fixed at 5% a year and there are no further contributions (according to the Nutmeg compound interest calculator).

The power of compounding

(£10,000 with 5% annual interest over 20 years)

The real-world implications of this “extra” amount could be significant. Remember that your retirement fund will hopefully be larger than £10,000 and be growing for decades.

Compounding might allow you to retire earlier than you first thought or to make memories with your family. Maybe you’ll be able to enjoy a more comfortable – or even luxurious – retirement lifestyle than you planned or incorporate world travel into your life after work.

Remember, the above figures are for illustration purposes only. Returns aren’t guaranteed and are unlikely to be consistent each year.

2. You don’t need to take any action to see its effects

One of the main benefits of compounding is that it doesn’t require you to do anything, and it costs nothing. You’ll simply need patience and a long-term focus.

This can be hard in an era of 24/7 rolling news, instant updates to your phone from social media, and a geopolitical landscape in flux. But staying calm and blocking out this extraneous noise is key.

Remember that your plan is individual to you and if your goals haven’t changed then your plan usually doesn’t need to either.

For compounding to work to your advantage, it needs time and money. You’ll need to start planning for your future as early as possible and, in the case of invested wealth, avoid kneejerk reactions during periods of volatility.

Withdrawing invested funds during a market downturn means that your money won’t be there if markets recover, which, historically, they have. Alongside this opportunity cost, your diminished fund will also lower the positive effects of compound growth.

3. Small, regular investments benefit from compounding

As with our magic doubling penny, the effects of compounding become increasingly pronounced as values rise, but it’s also completely normal to start small.

You might invest large lump sums or sudden windfalls, but regular savings and contributions can benefit from compounding too.

Say you invested £250 a month in the FTSE 100 with a 5% average annual return. After 12 months, you’ve invested £3,000 but generated just £83 in returns (according to Nutmeg’s calculator).

After 10 years, your total contributions have increased to £30,000. Your compound returns, though, have grown to £8,982.

By year 26, your fund will exceed £160,000. Your £250 monthly contributions now total £78,000 and have generated more than £82,000 in returns, pushing you beyond the compound investment tipping point.

3 times when compounding can negatively affect your finances

1. When you don’t understand it

The powerful effects of compounding can help to grow your wealth significantly over time. As Einstein might have said, “He who understands it, earns it…”. But the quote doesn’t stop there.

It’s important to remember the second half too: “He who doesn’t [understand it], pays it.”

Working with a financial planner can provide financial benefits as well as non-financial ones, like money confidence, a sense of control over your future, and an education in the oftencomplex world of finance.

Once you understand how compounding works in your savings and investments, you will be able to spot it working in other areas too (see points 2 and 3 below). Future Planning can help you mitigate the negative effects of debt and inflation.

3. When compounding affects the rising cost of goods and services

UK inflation measures the rising cost of goods and services over a specific period, usually a year. When price rises are recalculated, they begin from their current point. So, price increases due to inflation this year mean higher prices next year, and so on.

Say a product costs you £100 this year and inflation is at 5%. Next year, the same product will cost you £105, and this will be the starting point for future increases. This also compounds the decrease in your spending power.

After 10 years of inflation at 5%, your £100 will buy you around £62 of goods and services (in today’s prices).

2. When it applies to interest on debt

While compounding is quick to reward sound investment choices and money management, it can be destructive when times are harder. In the same way that compound interest can build up your savings, it can increase your debt.

Ideally, we’d use our 5% example again here, but where high-interest debt like credit cards is concerned, the interest you pay is likely to be much higher.

Imagine a £1,000 debt, with annual interest of 20%. In year one, your interest payment is £200. If you fail to pay off any of your debt, by year two you’ll be paying 20% on £1,200… And so on. We’ve already seen how quickly invested amounts can snowball, so it’s all too easy to imagine the speed with which your high-interest debt could spiral out of control.

You might be tempted to pay off only the minimum repayment amount each month, but this may be unwise. The longer you borrow for, the more interest you are charged, and the larger the amount you have to ultimately repay.

According to Barclaycard’s repayment calculator, if you borrowed £3,000 at age 21 and repaid only the minimum amount each month, it would take until you reached age 48 to clear your debt. That’s more than 27 years to clear £3,000 with interest totalling more than £4,700.

How to make the most of compounding

As we have seen, compounding can be an incredibly powerful financial process that can significantly boost your wealth but potentially harm it too.

Thankfully, there are several simple steps you can take to ensure you’re making the most of the compound effect, using it to make your money work for you.

Start early… But remember that it’s never too late to start

Compounding requires time and patience so begin your investment journey as early as possible. Be sure you have a definite goal in mind and then focus on that – this will help you to drown out the noise of geopolitics and the latest investment fads or trends.

Short-term volatility is an inherent part of investing, so the important thing is to remain invested.

Remember too that it’s never too late to start taking advantage of compounding. Your goal could be as little as five years away, so get in touch now if you think you’d like to start investing.

Concentrate on your budget and pay your future self first

A good budgeting habit to adopt is paying your future self first. This means making saving and investing a priority each month and then budgeting with the money that remains.

You might save or invest unexpected lump sum amounts – from a work bonus or inheritance, say – and you can also put aside pay rises.

Remember that small, regular sums can soon add up and the benefits of compounding will help them grow further.

As a side note, another benefit to this latter approach is that it effectively drip-feeds your investments, also known as “pound cost averaging”. This can help to smooth out the volatility we’ve already spoken about as it means you buy some shares or fund units when prices are low and some when prices are higher, effectively giving you an average of the market’s returns over time.

Understand your attitude to investment risk, and diversify

Compounding is powerful and over the long term, you might reach the compounding tipping point. But remember that this isn’t your objective – reaching your long-term goal is. Or to put it another way, investing isn’t a race.

That means understanding your attitude to risk and your capacity for loss and basing your investment decisions around these. You want to reach your goal as quickly as possible, but only while taking the amount of risk that is appropriate for you.

Diversifying your investments across asset classes, sectors, and geographical regions is an effective way to spread investment risk, keeping your wealth building as it takes advantage of compound growth.

Get in touch

While it’s impossible to know whether Einstein ever referred to compounding as the “eighth wonder of the world” the concept’s power is harder to refute.

As is the sentiment that “He who understands it, earns it, he who doesn’t, pays it.”

Compounding can have a hugely positive or negative influence on your long-term financial plan. So, whether you want help budgeting and managing debt, or you’d like to benefit from compound growth in your savings or investments, professional financial planners can offer invaluable guidance and support.

We might not be able to explain E=mc2 but we could help you reach your investment goals or clear your high-interest debt, helping you to live your dream lifestyle now and when you retire. Contact us now to find out how.

At Future Planning, we help Swindon clients build financial confidence, manage debt, and achieve long-term wealth growth. Contact us today to see how compounding could work for you.