There are many things we would like to leave for our loved ones when we pass away, from fond memories to heirlooms, but the one thing we don’t want to pass on is a hefty Inheritance Tax bill.

Inheritance Tax is generally known as ‘Britain’s most hated tax’ and it isn’t hard to see why. Thankfully, there are several things you can do to help lessen your Inheritance Tax burden, including making gifts during your lifetime. Here is everything you need to know about what the tax is, as well as what you can do to mitigate it.

A brief history of Inheritance Tax

Essentially, Inheritance Tax is a tax on the estate of a person who has passed away. This includes their money, property, and possessions.

Inheritance Tax has existed in one form or another since roughly the 17th century. It was first brought about in 1694 to help finance a war against France and, over the years, it has had various incarnations.

1694 Probate Duty

1780 Legacy Duty

1858 Succession Duty

1889 Estate Duty

1975 Capital Transfer Tax

1986 Inheritance Tax

How much tax will I have to pay?

According to a report published by HMRC, in 2017-18, only 3.9% of deaths in the UK resulted in an Inheritance Tax bill. This is because Inheritance Tax is not paid on the total value of your estate, but on the value of your estate above certain thresholds.

This threshold is known as the nil-rate band. For the 2020/21 tax year, this band is set at £325,000. On top of this there is also the residence nil rate band, which grants a £175,000 exemption and is conditional on the main residence being passed down to children or grandchildren. This brings the threshold up to £500,000.

If the value of your assets is higher than the nil-rate band, your estate may be liable for a 40% Inheritance Tax.

Here’s an example. If a person died with an estate worth £675,000 and left their main home to their child, they would typically pay Inheritance Tax on the value of their estate above the £500,000 threshold.

A 40% tax bill on this £175,000 would leave their family with a final tax bill of £70,000.

On the flip side, if the value of your estate does not exceed the thresholds when you pass away, your family would not need to pay any tax at all.

Note that there will be a tapered withdrawal of the additional nil-rate band for estates with a net value of more than £2 million. This will be at a withdrawal rate of £1 for every £2 over this threshold.

What tax benefits do couples get?

One notable exception to the rules regarding Inheritance Tax is that if you are married or have a civil partnership, your partner can inherit your entire estate without having to pay an Inheritance Tax bill.

Your partner also inherits any unused Inheritance Tax allowance when you pass away. This includes both the nil-rate band of £325,000 as well as the residence nil-rate band of £175,000. This means that if you didn’t use any of your allowance, they’d have an allowance of £1 million instead of just £500,000.

Gifting and Inheritance Tax

Inheritance Tax bills can be quite steep, but thankfully there are many ways in which your tax bill can be reduced.

Giving gifts is a simple way to reduce the value of your estate when you die, and to reduce the size of your overall Inheritance Tax bill.

Before we get into any of the details regarding gifting, it’s important to note that you should always keep accurate records whenever you are giving a gift. These records should include:

- What gift you gave

- Who you gave it to

- When you gave it

- How much the gift is worth

These records can help the executor of your will to work out the total value of your estate when you’ve passed away. If you do not, you may have to pay more Inheritance Tax than you should.

When gifting as part of estate and Inheritance Tax planning, there are two different kind of gifts. The first are those that are considered outside of your estate immediately. Others are potentially exempt depending on when they’re given and when you pass away.

What gifts are free from Inheritance Tax?

1. Potentially Exempt Transfers

Theoretically, you can give gifts of unlimited value, and they won’t be considered part of your estate for Inheritance Tax purposes, as long as you give the gift more than seven years before you die. These gifts are called ‘Potentially Exempt Transfers’ because they may be exempt from the value of your estate when calculating Inheritance Tax, providing you survive another seven years.

If you do not survive for the further seven years, then the value of the transfer is added to the value of your estate when calculating your tax bill. This is called the ‘seven-year rule’.

However, it’s also important to note that Potentially Exempt Transfers must meet certain conditions and are subject to exemptions. For example, you can only gift to another individual or into a trust, so a gift cannot be made to or from a company.

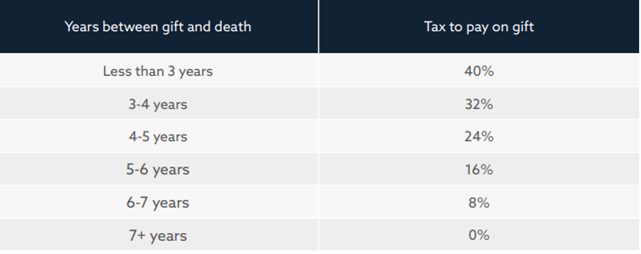

If you decide to make a sizeable gift but then pass away before those seven years are up, Inheritance Tax may be due. However, there is a sliding scale of the tax depending on how long before you died you chose to make the gift.

The table below shows the reduction in Inheritance Tax on the gift depending on how much time has elapsed:

If, however, you made the same gift but passed away four years and a month later, your estate would potentially have to pay Inheritance Tax but at the reduced rate of 24%, leaving you with a tax bill of £2,400.

2. Gifts to spouse or partner

One bit of good news is that you don’t have to pay Inheritance Tax on any gifts that you give to your spouse or civil partner. This means you can gift your partner as much as you like in your lifetime, as long as they live in the UK permanently.

Furthermore, married couples and civil partners are allowed to pass on their entire estates to their spouse tax-free when they pass away.

As we mentioned earlier, partners can also inherit their deceased spouse’s unused Inheritance Tax allowances.

For example, if a husband dies and leaves his entire estate to his wife, she can take his unused tax allowance and add it to her own.

3. Annual exemption

Each tax year (6th April to 5th April) you can give away £3,000 worth of gifts without their value being added to your estate. This is called your ‘annual exemption’

This exemption can be carried over from the previous year, but only up to a value of £6,000, so if you’re looking to use gifts to reduce the value of your estate, you need to carefully manage it.

4. Small gifts

You can give as many gifts of up to £250 to as many individuals as you like in any tax year. However, you cannot give one of these gifts to someone who has already received your whole £3,000 annual exemption.

5. Weddings

Marriages and civil ceremonies are another opportunity to give gifts tax-free and the amount that you can gift varies depending on who is getting married.

Typically, you can give a gift of up to £1,000 per person without the amount being included in the value of your estate.

However, this amount may be greater if you’re gifting to family. If a child is getting married then you can give up to £5,000 without it being added to the value of your assets, while you can gift up to £2,500 to a grandchild or great-grandchild.

6. Gifts from income

If you have enough income to maintain your usual standard of living, you can gift surplus income – for example, by paying it into a child’s savings account.

This can be a very valuable Inheritance Tax exemption, but it is also complicated and can potentially be disputed by HMRC. This is why it’s particularly important that you keep good records of your gift-giving if you’re planning to gift in this manner.

For this exemption to apply you must meet three conditions:

- The gift must be made out of income ‘taking one year with another’

- The gift formed part of your normal expenditure – this generally means that the gift should be regular in terms of value and frequency

- You should be left with enough income to maintain your standard of living

One of the tests that HMRC use to determine whether gifting in this way is allowed due to excess income is to see whether the gifts you give are regular. Typically, there needs to have been an established pattern of gift-giving to satisfy them that it is a normal expenditure. Because of this, if you do intend to gift in this way, make sure that you can maintain the regular payments, and keep good records.

For example, Mr Smith is 80 years old and retired. He has a steady income of £60,000 per year, consisting of pensions and investment income. He can save £2,500 per month or £30,000 per year.

For the last five years, Mr Smith has been making regular monthly gifts out of his surplus income of £1,000 per month to his son and daughter. As he has been giving the gift regularly for such a long time, HMRC will likely accept that this is a normal expenditure.

If HMRC does accept these gifts are part of his normal expenditure, Mr Smith will still be able to make use of his annual £3,000 Inheritance Tax allowance.

Leaving gifts in your will

If you want your money to go to a good cause after you die as well as reducing your Inheritance Tax bill, you may want to consider leaving some of your money to charity in your will.

To encourage more people to give money to charity, any cash or asset that you leave to a charity, either during your lifetime or in your will, will be exempt from Inheritance Tax.

Furthermore, leaving money to a charity in your will can reduce the overall amount of Inheritance Tax that is due on your estate. This can potentially also bring the value of the estate below the threshold of the nil-rate band, in some cases.

If you leave at least 10% of your estate to charity in your will, the government will reduce the amount of Inheritance Tax you have to pay, meaning that you will pay a 36% tax instead of a normal 40%.

This can mean that not only would you be helping a charitable cause, but you could save a significant amount on your tax bill.

Reliefs when gifting certain assets

- Business Property: If you own a business, you may be eligible for Business Property Relief, which can reduce the value of a business property by up to 100% when it’s being transferred. This transfer can be made in life or as part of a will, as long as the business has been owned for at least two years.

- Agricultural Property: If you own a farm, you can pass it on free from Inheritance Tax, although it must meet certain conditions. Certain farm assets, such as agricultural machinery, are also not exempt.

- Woodland Property: Woodlands used for commercial purposes can potentially get Inheritance Tax relief of up to 100%. If the land is used for timber, the tax can also be postponed until the trees are felled, provided that you have owned the woodland for five years prior to your death.