Buying your first home is a huge decision and a milestone you may have been looking forward to for years. But it can be a daunting step to take too.

Rising property prices mean UK adults are taking their first step onto the property ladder later in life. The average first-time buyer in the UK is 34, according to Money research. Over the decades, the average age has increased as more young people go to university and face obstacles when saving a deposit or taking out a mortgage. However, Brits are far from the oldest average first-time buyer in the world; in Switzerland, the average first-time buyer is 48.

If you’re thinking about buying your first home, there are lots of things to consider and steps you need to take. Whether you’re perplexed by the jargon or aren’t sure how the homebuying process works, this guide will help lead you through buying your first home.

The deposit: How much do you need and what are the best ways to save?

The first hurdle to buying your first home is usually saving a deposit. Traditionally, you need a deposit of 10% of the property’s value to put down.

Rising house prices have made this step more challenging than ever. With the average house price exceeding £250,000, it’s not uncommon for first-time buyers to need to save £25,000 or more. Before you set a saving goal, you should research your local property market and consider what type of home you want. This means you can set a clear target for your deposit, but keep in mind that prices could rise further.

Saving a deposit can seem like a huge challenge, but there are steps you can take to stay on track.

1. Review your current budget

Your first step should be to review your current income and expenditure. Are there any changes you could make that mean you’re able to save more? Even a small amount regularly going into your savings account can add up over time and mean you’re able to buy a home sooner.

2. Break your deposit down into smaller goals

Setting out a goal to save £25,000 can be daunting. Rather than focusing only on this end goal, break it into small targets. How much do you want to save each month? How much do you want to save this year? By setting smaller targets, it can help you track the progress you’re making and the positive steps you’re taking. Make sure you’re realistic. Setting overly ambitious goals that you’re likely to miss can be disheartening and knock you off track.

3. Pay yourself first

Rather than waiting until the end of the month to add to your savings, make it a priority. Make your savings part of your monthly expenses and move the money straight into your savings account when you’re paid.

The 5% mortgage guarantee

A government-backed mortgage scheme could help you buy sooner by encouraging more lenders to offer 95% mortgages. This means you need a deposit of 5%, rather than the traditional 10%.

The scheme is available from a range of high street lenders, and you can use it to purchase a home up to the value of £600,000. From a buyer’s perspective, the mortgage would operate in the same way as any other mortgage.

The scheme will run until December 2022.

4. Find the right place to save

Where you decide to save your money can make a huge difference to how quickly you reach your goal. While interest rates are generally low, even a small difference can have an impact.

If you’re certain about buying a home, saving through a Lifetime ISA (LISA) makes sense. You can deposit up to £4,000 into a LISA each tax year and will receive a 25% government bonus. That means you could have up to £1,000 added to your deposit each year.

To open a LISA, you must be aged between 18 and 39, although you can continue making contributions until you’re 50. However, if you withdraw money before the age of 60 for a purpose other than buying your first home, you will lose 25% of the amount withdrawn.

While you can’t open a Help-to-Buy ISA anymore, if you already have one, you can continue to make contributions until November 2029. You can pay in up to £200 a month, and you’ll receive a 25% government bonus, up to a maximum £3,000, when you buy your first home.

Will you be receiving help from the Bank of Mum and Dad?

Receiving help from parents has become common among first-time buyers. In 2020, Legal & General suggested half of first-time buyers under 35 received some financial support from family. If your family is a in a position to provide a lump sum, it can relieve some of the pressure of saving a deposit. However, make sure you’re all on the same page. For example, is the money a gift or a loan?

Your family doesn’t need to have a lump sum to be able to provide a helping hand. A family offset mortgage, for example, could mean they’re still able to earn interest on their savings while reducing the amount of deposit you need. If you’d like to discuss these options, please contact us.

Help-to-Buy Equity Loans: Reducing your deposit and mortgage

The Help-to-Buy Equity Loan scheme is a government scheme that could reduce how much you need to save for a deposit and the size of your mortgage.

If you use this scheme, you’ll need a minimum of a 5% deposit. You can then borrow an equity loan that covers from 5% to 20% of the property purchase (up to 40% in London) and take out a mortgage on the remaining amount. It can make buying a home more affordable.

However, you need to keep in mind that you will need to repay the loan alongside your mortgage. You do not have to pay interest on the loan for the first five years. If you sell your home, the loan must be paid back in full and, as it’s an equity loan, the amount may increase if the value of your property rises.

The scheme is open to all first-time buyers over the age of 18 who pass affordability checks. The property you buy must be used as your main home and must be a new build sold by a Helpto-Buy registered homebuilder. The maximum you can borrow through the scheme depends on where you live.

The Help-to-Buy Equity Loan scheme can be useful for first-time buyers, but it’s important you understand the pros and cons before making a decision.

How much can you borrow through a mortgage?

Before you start searching for your home, you need to understand how much you can borrow through a mortgage.

There are many factors that will influence a lender’s decision. A general rule of thumb is that you can borrow up to 4.5 times your annual income.

Obtaining a mortgage in principle is one way to get a clearer idea. A mortgage in principle provides an indication of the amount a lender will offer you based on details you’ve provided. The lender may conduct a soft credit check, but this will typically not affect your credit score.

You can often complete the application online and receive a response in just a few minutes. Some estate agents will want to see a mortgage in principle when you make an offer, so it’s a step worth taking. Most mortgages in principle will last for three months.

While useful, keep in mind that a mortgage in principle is not a guarantee. Nor do you have to take out a mortgage with the same lender you have a mortgage in principle from.

While a lender will complete affordability checks, it’s worth reviewing your own finances to provide peace of mind too. Make sure you’re comfortable with the potential outgoing and the impact it will have on your budget.

Finding the right mortgage for you

- Repayment mortgage: This is the type of mortgage most homeowners will take out. Your monthly repayments cover the interest and a portion of the debt. Assuming you keep up with repayments, you will own your home at the end of the term.

- Interest-only mortgage: With this type of mortgage, you will only make payments to cover the interest on the loan. Your monthly repayments will be lower, but you’ll still owe the full amount borrowed at the end of the term. As a result, this type of mortgage is becoming less popular.

- Fixed-rate mortgage: With this option, the interest rate will be fixed for a set period, usually two, three or five years. You will know how much your repayments will be each month during this period, providing certainty, but you will not benefit if interest rates fall.

- Tracker mortgage: A tracker mortgage follows the Bank of England’s base interest rate. This means your interest rate could move up or down. So, you’d benefit from a lower rate if the base rate fell, but your outgoings would rise if the base rate increased.

- Variable mortgage: This option is similar to a tracker mortgage, but will follow your lender’s rate of interest, rather than the Bank of England’s. This means your repayments can rise and fall.

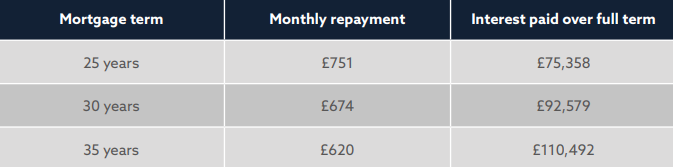

Source: Money Saving Expert

As well as interest and regular repayments, there are other things you need to think about when taking out a mortgage, including:

- Mortgage fees or charges

- Whether you can make overpayments

- The ability to port your mortgage to another property.

With so many different things to think about and multiple lenders to consider, including those without a high street presence, it can be difficult to choose a mortgage lender. This is where a mortgage broker can help you.

A mortgage broker will help you identify which lenders are likely to approve your mortgage application and help you access the right deal for you. They can also help you get your paperwork in order, speeding up the process, and answer any questions you may have.

7 tips to improve your chances of securing a mortgage

1. Know what you can afford

Understanding how much you can afford to borrow is important. It might be tempting to ask to borrow more, but if it’s viewed as unaffordable, your application will be rejected. Be realistic when looking for a home and applying for a mortgage.

2. Demonstrate a regular income

You will need to demonstrate how you’ll meet mortgage repayments. Usually, this will mean sending several payslips to show a reliable income. If you’re self-employed, you need to make sure your accounts are up to date. Make sure you have all the necessary paperwork to hand.

3. Review your credit rating

Lenders use your credit report to assess how likely you are to default on your mortgage. You can review your own credit score and report for free, and it’s worth checking if the information is accurate and whether lenders could find some red flags. There may be some simple things you can do to boost your credit score, like registering on the electoral roll.

4. Reduce unsecured debts

If you have debt, reducing it as much as possible can help you secure a mortgage. This may include reducing the amount you owe on credit cards or loans. A lower debt-to-income ratio provides you with more disposable income and reduces the risk you’ll default on your mortgage. This can give lenders confidence.

5. Don’t apply for new forms of credit

While it might be tempting to apply for new credit when buying a home, to pay for furniture or decorating, for instance, try to avoid this. Applications for credit show up as a hard search on your credit report. This means a mortgage lender will be able to see it. Recent or multiple applications can put a lender off as it may suggest you’re rapidly increasing how much debt you have.

6. Be mindful of your money habits

It’s common for lenders to review your recent bank statements when assessing your application. They’re not going to reject your application if you’ve eaten out or treated yourself to some new shoes, but there are some red flags they’ll be looking for. If you regularly go into your overdraft, money is going out to gambling companies, or you use payday lenders, it could harm your application.

7. Choose the right lender

If one lender rejects your application, it doesn’t mean they all will. There is a range of lenders, including specialist ones, that may be suitable for you. Choosing the right lender is important. As a previous application will show up on your credit report, you should carefully assess lenders before applying. A mortgage broker can identify lenders that you match the criteria of.

Do you need to consider financial protection now?

Financial protection can help provide a regular income or a lump sum when you need it most under certain circumstances. When you’re taking out a mortgage, it’s a good time to think about if financial protection could be right for you. It could help you keep up with repayments if you became too ill to work or were involved in an accident. If you’d like to discuss what your options are, please contact us.

The home-buying process

When buying property for the first time, you may not know what steps need to be taken or when. It can mean you’re left feeling unsure of what to do and who to speak to about different parts of the process. This timeline can help you understand how things progress.

Do you need to pay Stamp Duty?

Stamp Duty is a tax paid when buying property. Most first-time buyers will not need to pay Stamp Duty.

In England and Northern Ireland, first-time buyers paying £300,000 or less do not need to pay Stamp Duty. If you’re buying a home worth between £300,000 and £500,000, you will need to pay Stamp Duty at 5% on the amount above £300,000. If you’re purchasing a home above £500,000, you will need to pay Stamp Duty at the normal rate.

Even if Stamp Duty is not due, you will still need to complete a form within 14 days of completion.

In Scotland, first-time buyers do not need to pay Land and Building Transaction Tax if they are buying a home for less than £175,000, this compares to the usual £145,000 threshold.

There is no first-time buyer’s relief in Wales. You will need to pay Land Transaction Tax if you’re buying a home for more than £180,000.

Lending you support throughout the process

If you’re a first-time buyer, we know that buying a home can seem complicated and scary. We’re here to offer advice and support throughout the process. If you’d like to talk to us, please contact us.

Please note: This guide is for general information only and does not constitute advice. The information is aimed at retail clients only. Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.