Your home may be one of the largest assets you have. With property wealth often inaccessible, you may be considering using equity release to unlock some of the money tied up in your home.

It could be a valuable way to boost your finances in your later years.

Each equity release provider will set their own criteria. However, to be eligible, you’ll usually need to be aged at least 55 and the property must be your main home. Your age and the value of your home will affect the amount you can release.

You can use equity release if you have a mortgage. You must use the money released to pay off any outstanding debt that’s secured against your home, including a mortgage or loans, along with any early repayment fees.

If equity release is something you’re interested in and want to understand if it could be right for you, read on.

Equity release is similar to a loan secured against your home

There are several different types of equity release. The most common is a “lifetime mortgage”.

A lifetime mortgage is similar to a loan secured against your home. However, rather than making regular repayments, the amount you owe, along with any interest accrued, is usually rolled up. The debt will be paid when you move into long-term care or pass away.

As a result, a lifetime mortgage could be a useful way to boost your finances now without increasing your regular expenses.

You can receive the money you release as a one-off lump sum or regular smaller payments. You may also be able to mix the two options.

While it might seem like a straightforward way to fund retirement or other plans you have in your later years, there are drawbacks you may want to consider first.

Home improvements are the most popular way to use equity release money

You can use the money you access through equity release however you wish.

A survey published in This Is Money revealed 39% of people spend at least some of the money improving their home. Other common reasons include funding holidays, retirement, or gifts to family.

It could also provide a useful way to pay off debt as you near retirement. 33% of equity release customers used the money in this way. On average, they spent £18,441 clearing debt.

A mortgage or other type of debt could affect your retirement plans. According to PensionBee research, almost half of people over the age of 55 who are paying off a mortgage are worried about being able to meet their repayments and how they’ll repay their loans in full.

Rising property prices mean more homeowners could be paying their mortgage as they near retirement in the future.

Equity release may provide a way to keep retirement plans on track and reduce outgoings once you give up work.

4 potential benefits of using equity release

1.You can release a tax-free lump sum

The obvious advantage of using equity release is that it gives you money you can spend how you like now.

House prices have increased over the last few decades – the average property price was almost £280,000 in August 2023, according to Halifax’s House Price Index. Equity release could give you access to a significant lump sum that would otherwise be locked away. It’s a way to take advantage of rising property prices without having to sell your home.

2. You may be able to access further money in the future

As well as taking a lump sum through equity release, you could also opt for a drawdown lifetime mortgage. This would allow you to make further withdrawals in the future.

According to the Equity Release Council, 52% of customers opted for a drawdown lifetime mortgage in the second quarter of 2023. On average, homeowners using drawdown take 55% of the available cash upfront, leaving a sizeable amount to draw on in the future if they need to.

Using a drawdown lifetime mortgage might suit your needs if your long-term plans would require an additional cash injection.

Knowing that you could withdraw more if you faced a financial shock could provide peace of mind too.

3. You don’t need to make repayments

If you want to access additional money, many of the alternatives will require you to make regular repayments. This might not fit into your budget or align with your goals.

As a result, equity release may be a useful option if you want to release money without increasing your outgoings.

4. You can remain in your own home

One of the most attractive benefits of equity release for many people considering it is that you don’t need to move out of your home.

You might have an emotional attachment to your property, which means you don’t want to downsize. Or the location may be close to amenities or loved ones, which means it’s perfect for you.

4 possible drawbacks of using equity release

One of the benefits of equity release is that you don’t have to make repayments. However, it also means the amount you eventually owe could be much higher than the money you’ve withdrawn from your property.

If you don’t make repayments, the interest is added to your balance. The following month or year, depending on your plan, the interest will be calculated based on the amount you borrowed, plus the interest that has already been accrued.

As a result, the interest that is added each month or year could rise, even if the interest rate remains the same.

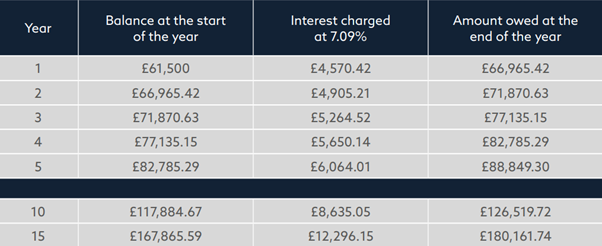

The below table shows the effect of compounding interest. In this scenario the homeowner has used equity release to access a one-off lump sum of £61,500, the interest is added monthly, a oneoff fee of £895 is added to the balance in the first year, and no repayments are made.

Source: Equity Release Council

As the example shows, the amount of interest added each month will rise due to compounding. So, it’s important to be aware of how the amount you owe could increase.

You can see that, by the end of year 15, compound interest means that the amount owed is approaching three times the original amount borrowed.

Many equity release providers allow you to make repayments or pay off the interest if you choose to. This could help you manage the debt, but you may want to calculate how it could affect your outgoings.

If you’re considering equity release, you can ask for a personalised illustration, which would show how the amount you owe could rise during your lifetime and help you understand if it’s the right decision for you. It could take into account the amount you’re borrowing, the interest rate you may be offered, and whether you plan to make repayments.

2. It may affect the inheritance you leave behind

If leaving an inheritance behind for your loved ones is important to you, equity release may not be the right option.

Equity release could reduce the value of your estate and what you leave to family and friends. It may mean your family don’t inherit your home, so it’s worth thinking about how you’d like your assets to be distributed before you use equity release.

Often, equity release providers have a “no negative equity guarantee”. This means the total amount you owe cannot exceed the value of your home. So, you could still pass on other assets to your loved ones.

3. It might limit your options in the future

Once you’ve used equity release, you will not usually be able to secure other loans against your home. If you wanted to access further borrowing in the future, it could limit your options.

It’s not impossible to move home once you’ve used equity release, but it can make it more difficult. As the money you’ve accessed is secured against your home, you could find you don’t have enough equity to purchase a new property.

Setting out your long-term plans before you use equity release could help you understand if it may affect them.

4. It can affect means-tested benefits

As means-tested benefits may consider the value of some of your assets, such as savings, releasing a lump sum from your property could affect your income.

You might want to consider how equity release could affect the benefits you receive now or in the future.

Useful alternatives to consider if you’re thinking about using equity release

It’s important to weigh up the alternatives to equity release if it’s something you’re thinking about. You may find a different solution makes more sense for you.

Here are five options that, depending on your circumstances and goals, could be worth weighing up.

Downsize

Selling your current home and purchasing a cheaper one could release some of your property wealth. It may also provide an opportunity to buy a home that will suit your long-term needs.

Of course, there are disadvantages too. As well as the potential drawback of moving away from your community, downsizing could also come with costs.

Take out a loan

If you want to boost your wealth now, a loan might be suitable.

You might need to consider the effect it could have on your budget, and your income will affect your options. However, assuming you keep up with repayments, it means you could still pass on your home to loved ones when you die.

Remortgage your home

It may be possible to borrow more against your home through a traditional mortgage. So, if you were considering equity release to access money to fund home improvements or a holiday, it might be right for you.

Your mortgage lender will consider your affordability, including your income and retirement age. As the outstanding amount on your mortgage will increase, your repayments are likely to rise.

Take out a retirement interest-only mortgage

If you’re worried about paying your mortgage into retirement, an interest-only mortgage could be an option.

As you’ll only be paying the interest off each month, your outgoings would be lower when compared to a repayment mortgage. However, keep in mind that interest rates can change and may affect your payments.

Assuming you keep up with payments, the amount you owe on your mortgage would remain the same and would be repaid when the property is sold or you pass away.

Use other assets

Before you decide to use equity release, you may want to review your other assets. You might find your pension, investments, or savings could provide the boost to your finances you want.

Assessing the long-term effect of depleting other assets through a financial review could give you confidence to use them to reach your goals.

Contact us to discuss if equity release could be an option for you

If you’d like to learn more about equity release and understand if it may support your goals, we could help.

Please contact us if you have any questions or would like to arrange a meeting.

Book a free consultation with Future Planning to discuss your financial goals and take the next step toward a secure future.

Please note: This guide is for general information only and does not constitute advice. The information is aimed at retail clients only.

Think carefully before securing other debts against your home.

A lifetime mortgage is a loan secured against your home. To understand the features and risks, ask for a personalised illustration. Equity release will reduce the value of your estate and may affect your entitlement to means-tested benefits. Your home may be repossessed if you do not keep up repayments on your mortgage.