When building a financial plan, investing often plays a central role. While modern technology has become crucial for investing, it’s a practice that’s been around for centuries, and we can still learn from the past.

Investing can provide you with an opportunity to grow your wealth. Rather than depositing money into a savings account to earn interest, which has been low for the last decade, investing has the potential to deliver higher returns. Of course, this comes with investment risk and the value of investments can fall as well as rise. However, with a long-term view that considers risk, it can help you reach your goals.

Improving returns, coupled with businesses needing a capital injection, was the driving factor behind the start of investing, too.

Laying the foundations in 17th century Europe

There is evidence that investing took place millennia ago. The Code of Hammurabi, which was written around 1700 BCE in what is now modern-day Iraq, includes the first known framework for investing. But this framework differs from modern-day investing as it sets out a way to pledge land as collateral when investing in a project.

To find the roots of modern-day investing, you don’t have to go back quite as far

In the 1600s, shipping had become big business. British, Dutch, and French ships were regularly making the voyage to the East Indies and Asia to bring back goods from the East, from spices to silk.

While there was a demand for these goods, the voyages were risky. As a result, ship owners sought investors to fund the voyage and investors would receive a percentage of the proceeds if the trip was successful. To spread risk, investors would put their money into several different voyages.

Eventually, shipping companies formed. So, rather than investing for a single voyage, investors could purchase stocks and benefit from returns across all the voyages a company undertook, helping them to spread risk. Many of these “East India” companies benefited from royal charters that limited competition, leading to significant profits.

At this point, stocks were a physical piece of paper that could be bought and sold. However, with no stock exchange, finding a buyer could be difficult. Brokers and coffee shops to facilitate this emerged, but it wasn’t too long until stock exchanges provided a solution.

Romans paved the way for pension funds

Your pension is probably among your largest investments.

Pensions have their origins in the Roman empire when Augustus Caesar worried that retired soldiers may rise up against him.

So, a pension lump sum was paid when they retired. While these were the first pension, they were still a long way off from pensions as we know them today.

The Amsterdam Stock Exchange (now known as “Euronext Amsterdam”), which opened in 1602, is often regarded as the predecessor to the stock exchanges used today. A lot has changed in the last 400 years, but the basic principle remains the same: to connect investors with investment opportunities.

It took almost 200 years for the first stock exchange to open in the UK. The London Stock Exchange opened in 1801, but it can trace its roots to Jonathan’s Coffee House, which published stock and commodity prices, in 1698, and an unregulated “Stock Exchange” in Sweeting’s Alley in the 1700s.

Stepping into the modern world

While the concept of investing has remained the same, how investors invest has changed enormously. And technology has played a huge role in that. It’s now possible to invest wherever you are with just a few taps on your phone. It means investing is more accessible than ever.

Investors have more choice too. You can still invest in a single company if you wish. But you can also invest through funds that invest in a range of companies, helping you to spread the investment risk.

Some investment funds provide a way for people to invest without having to make day-today decisions, with a fund manager overseeing how the fund invests with particular targets and risk profiles in mind.

Sophisticated algorithms are also playing a role in the stock market. Stock exchanges now execute trades in less than half a millionth of a second, far faster than a human mind can make a decision. Instead, these decisions are based on careful calculation programmed into a computer designed to take advantage of tiny movements in the stock market. This is known as “high-frequency trading”.

So, how can investors compete with this? While human investors can’t keep up with the speed of algorithms, a long-term investment strategy can still deliver returns. Buying stocks or investing in a fund that matches your risk profile and holding these over the long term is a strategy that remains suitable for many investors.

Are Brits missing out on investing opportunities?

While investing can help you grow your wealth and is more accessible than ever, figures suggest many Brits are missing out.

In 2019, just 2.2 million, around 3% of people in the UK, were subscribed to a Stocks and Shares ISA, which provides a tax-efficient way to invest.

Source: HMRC

The ups and downs of the stock markets

Given the long history of investing, it’s inevitable that there have been ups and downs in the stock markets.

Today’s investors may remember the impact of the dot com bubble, the 2008 financial crisis, and, more recently, the Covid-19 crisis on their portfolio. The value of stocks falling isn’t new, and investors over the centuries have weathered the ups and downs as well.

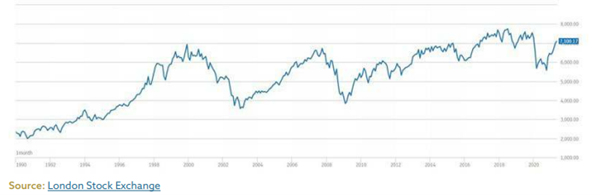

However, what past stock market data shows us is that, historically, markets do recover. The FTSE 100, which was founded in 1984, is a share index of the 100 largest companies listed on the London Stock Exchange. Over almost four decades, the FTSE 100 has experienced numerous “crashes” and “corrections”, but when you look at the long-term trend, markets have recovered.

In January 1990, for instance, the FTSE 100 value was 2,337. In May 2021, it had increased to over 7,000. The graph below demonstrates how the market has risen and fallen over the years, but investors that took a long-term view and held stocks despite falls would have benefited.

What causes a stock market crash?

No investor wants to experience a stock market crash, but they are a part of investing. Over the years, numerous factors have caused crashes, as these examples highlight:

- Perhaps the most famous stock market crash, the 1929 Wall Street Crash had an enormous impact and played a role in the Great Depression in the US. After nearly a decade of the stock market rising during the “Roaring Twenties”, some people began borrowing to invest, aiming to benefit from high returns. As investors began to cash out, the market dropped significantly on 29 October 1929, when investors sold more than 16 million shares on the stock market.

- The Black Monday crash of 1987 affected stock markets around the world, including New York, London and Hong Kong. A range of factors played a role in this crash, including oil prices following growing tension in the Middle East. It was also linked to newly introduced automatic trading systems, which allowed brokers to place bigger orders faster, causing company valuations to rise to excessive levels. The US Dow Jones stock index fell almost 22% in a matter of hours.

- In the 90s, so-called “dot com” stocks that invested in internet stocks were booming. As technology grew, more investors poured their money into these investments, leading to the dot com crash of 1999/2000, where some tech companies became overvalued, and eventually led to a crash.

- The financial crisis of 2008 is a crash many investors today will remember. The crisis began with subprime mortgages in the US, leading to banks taking on increased levels of risk and homeowners defaulting on their debts. The extent of the damage became clear when in September 2008, when Lehman Brothers, one of the world’s largest investment banks, collapsed. The impact spread throughout global stock markets and triggered a global recession.

5 investment lessons you can learn from the past

While past performance isn’t an accurate indicator of future performance, there are still key investment lessons you can learn from history.

1. Don’t try to time the market

As mentioned above, there are a huge number of things that can affect the value of stocks. Consistently predicting market movements is impossible, even for professionals with vast resources.

In the early 1600s, we doubt investors thought tulips would lead to a speculative bubble, but that’s exactly what occurred in the Netherlands in 1637. In modern times, few would have thought a global pandemic would sweep across the globe in a matter of months affecting a huge range of businesses as it did in 2020. The unexpected can, and does, happen.

As a result, trying to time the market can mean you end up missing out. According to Schroders, if you invested in the MSCI Global Index between 2001 and 2019 you’d have received average returns of 6.1% over the 19 years. However, if you tried to time the market and missed out on just the ten best days, returns would fall to 2.9% a year.

2. Focus on your long-term goals

The stock market experiences up and downs, and it can be tempting to focus on their daily movements. But if you’re investing for the long term, the long-term trend is far more important to focus on. As seen above, while market values have fallen in value at different points throughout history, they have recovered. The long-term trend is an upwards one. Over time, the peaks and troughs smooth out to show a gradual increase.

If you’re investing for a long-term goal, the bigger picture is more important than how a stock performs day-to-day.

3. Understand your risk profile

While the long-term outlook is crucial, it’s also important to recognise how much risk is appropriate for you. Your risk profile should consider a range of factors, from the other assets you hold to your overall attitude to risk. Understanding your risk profile can help you create an investment portfolio that reflects you and your wider financial plan.

While some investment can be tempting, understanding how much risk is involved before parting with your money is crucial.

4. Spread the risk you take

All investments come with some level of risk, but you can manage risk by spreading out investments across multiple companies, assets, sectors, and geographical locations. This is known as “diversifying”.

Early investors might not have had as much choice as investors today, but they still understood the importance of not putting all their money on a single venture. Investors supporting the first shipping voyages would often invest in multiple voyages at the same time to reduce the chance of losing all their money. The desire to spread risk is what led to the establishment of shipping companies. Today, diversifying is still important.

Spreading investments across multiple industries can mean that should one area suffer a dip, other investments can help balance this out.

5. Don’t follow the crowd

When investing, it can be hard to focus on which opportunities suit you rather than listening to what others are doing, whether you’re talking to friends or reading the newspaper. But simply following the crowd, rather than carefully weighing up your options and taking your time to research, can mean you make decisions that aren’t right for you.

Looking back 300 years, the South Sea Bubble highlights why following the crowd can be disastrous.

In 1720, the South Sea Company was granted a monopoly on trading with South America. As tales of unimaginable riches began to circulate, shares immediately rose by ten times their value. Understandably, investors wanted a piece of this, but speculation ran wild and some investing in companies was fraudulent or overly optimistic. When the bubble popped it caused a severe economic crisis and left many investors destitute.

With the benefit of hindsight, it can be easy to question how so many people got swept up in the bubble, but following the crowd is still an investment phenomenon that occurs today.

Putting past lessons into practice

While you can learn investment lessons from the past, it can be hard to put them into practice when it comes to your own investment portfolio. If you’d like advice and support to build a portfolio that reflects your goals and risk profile, please contact us.