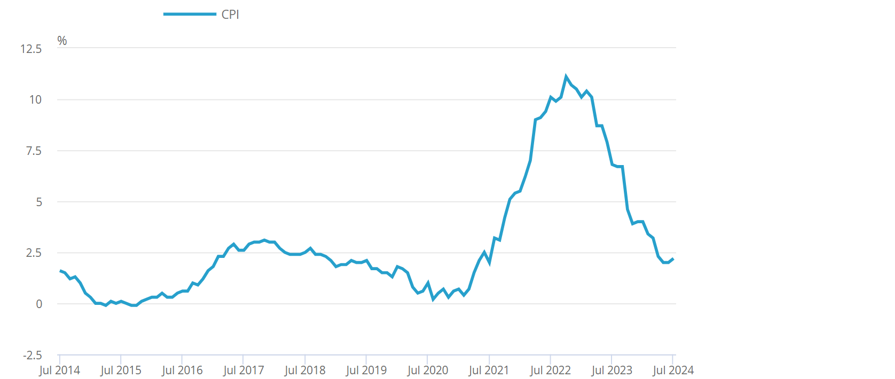

Back in the summer of 2021, after months of lockdowns, Covid restrictions finally lifted and inflation soared. The Consumer Prices Index (CPI) peaked that October, reaching a 41-year high of 11.1%.

The Bank Of England (BoE) – charged with keeping inflation close to its own 2% target – was forced to act. They did so using one of the main tools at their disposal: the base rate.

From an all-time low of 0.1% in December 2021, the rate was raised 14 times in the months that followed, peaking at 5.25%.

Fast-forward to summer 2024 and inflation is much closer to target. Accordingly, the MPC voted to reduce the base rate for the first time in four years.

Keep reading to discover what a rate cut might mean for your savings, investments, and your mortgage.

The Bank of England uses the base rate to help control inflation

As we have seen over the last couple of years, high inflation leads to rising bills and grocery costs and can leave UK households struggling. The cost of living crisis has hit families from across the wealth divide.

With inflation high, the BoE increased rates to encourage saving and reduce consumer spending, thereby reducing demand and slowing price rises.

The Office for National Statistics (ONS) confirms that for May and June, inflation reached and then stayed at the BoE’s 2% target.

Source: ONS

Despite a slight rise to 2.2%, forecasters are hopeful that the base rate could fall again before the end of the year.

You might find that your bank savings rate falls, making investing more tempting

Savers have had a tough time of it for the last decade or so. The situation was made worse as inflation rose. That’s because the CPI was above the average savings rate, meaning that your savings were effectively losing value in real terms.

More recently, as the base rate has increased and inflation has dropped, bank interest rates have improved. When bank rates are higher than the rising cost of living, you’ll see your cash begin to grow in real terms.

If the BoE continues to cut the base rate, high street banks will effectively pass this on to customers through falling savings rates. As always, it’s important to shop around for the best rate.

A high street bank might be a good choice for holding an emergency fund. That’s because you could need this cash at short notice. But more tax-efficient vehicles, including some types of investment, could be better suited to providing long-term growth if the savings rate continues to fall.

Your investments could also benefit from a falling base rate as business borrowing costs fall

When base rates fall, borrowing becomes cheaper. This is good news for your mortgage (more on which later), but it can be a boost to the wider stock market too.

When it’s cheaper for businesses to borrow, they can afford to invest in their own development, promoting growth. Lower borrowing costs also give you, the consumer, more to spend, helping to boost business profits.

If you have long-term goals, at least five years away, you might consider moving some of your cash savings into investments.

A Stock and Shares ISA, for example, is incredibly tax-efficient. Any gains you make are free of Capital Gains Tax, Dividend Tax, and Income Tax.

You’ll need to think carefully about your risk profile, capacity for loss, and time frames. But we can help here, so be sure to get in touch if you are concerned about your falling savings rates.

A falling base rate could mean your mortgage payments fall

First off, the bad news. If you’re on a fixed rate, a falling base rate won’t affect the cost of your mortgage repayments. At least, not yet. You might, though, find a better deal is available when the time comes to renew.

If you’re on a variable rate or tracker rate, though, you may find that your mortgage payments drop too.

A tracker rate should “track” the base rate, resulting in a slight fall. Your variable rate, meanwhile, may well change, but this will be reliant on your lender passing the base rate drop onto its customers.

If you have a mortgage deal that is due to expire soon, be sure to shop around and line up the best possible new deal.

Get in touch

If you would like to discuss any element of your long-term financial plans, including what global economic changes might mean for you, please email enquiries@futureplanningwm.co.uk or call 01793 575553.

Please note

The value of your investments (and any income from them) can go down as well as up and you may not get back the full amount you invested. You could lose your investment. Past performance is not a reliable indicator of future performance. Levels, bases of and reliefs from taxation may be subject to change and their value depends on the individual circumstances of the investor.

This article is for information only. Please do not act based on anything you might read in this article. All contents are based on our understanding of HMRC legislation, which is subject to change.