Buy-to-let properties can provide an additional income stream and help you to support your goals.

Becoming a landlord is something you may have thought about for a variety of reasons. You may want to purchase a buy-to-let property to diversify your assets or provide children with an inheritance. One of the most common reasons is to fund retirement.

In fact, according to the government’s English Private Landlord Survey 2021, 54% of landlords view their buy-to-let property as a “long-term investment to contribute to their pension”.

However, it’s also common to have concerns about buy-to-let. You may worry about understanding the regulations and tax requirements if you become a landlord.

If you’re thinking about investing in a property, there are some important things to consider first. Read on to find out what you need to know.

The 2 ways buy-to-let can support you financially

If you’re purchasing a property, it can provide you with an income stream and act as a longterm investment.

1.Rental yield

When someone is living in your buy-to-let, you’ll benefit from rental income. How much you receive will depend on a variety of things, from the property to whether you’ve decided to use a letting agent.

According to Zoopla, rental growth reached a 13-year high at the end of 2021. In the final quarter of the year, average rent increased by 8.3% to £969.

You will need to factor in periods when the property may be empty, as well as outgoings like mortgage repayments and maintenance costs. However, letting out a property can still significantly boost your income.

2. Property value

Historically, property has risen in value. So, if you purchase a buy-to-let property and sell it at a later date, you could make a profit.

Figures from Land Registry show that the average property in the UK in January 2002 was worth £97,623. Two decades later in January 2022, the price increased to £275,743. As a result, property can act as a long-term investment, but you should keep in mind that growth cannot be guaranteed.

Have you considered the risks of a buy-to-let property?

While a property can add value to you, there are risks to consider too. These could reduce the profitability of a buy-to-let property and can be timeconsuming to deal with.

For example, void periods, where there is no tenant, could mean you won’t be receiving an income from the property. During void periods, you’d still need to meet your own financial commitments, like mortgage repayments. So, it’s important that you have a financial safety net to fall back on.

In addition, there are tenant-related risks to consider. For example, what would happen if a tenant stopped paying rent or left the property in a state that wasn’t fit to rent to someone else?

You can take out landlord insurance to provide some protection in these instances. Yet, it’s important to understand the effect these circumstances could have before you jump into buying a buy-to-let property.

5 important things you need to know about buy-to-let mortgages

Many people that want to purchase a buy-to-let property will need to take out a mortgage to do so, and it’s essential that you understand how they work.

You cannot purchase a buy-to-let property with a normal residential mortgage.

Even if you’ve taken out a mortgage to buy a home before, there are some important differences that you may not know about.

Here are five things you need to know if you’ll be taking out a buy-to-let mortgage.

If you’ve become an “accidental landlord” – for example, if your circumstances have changed or you’ve inherited a property and have a mortgage on it – you must let the lender know or it could invalidate your mortgage.

1. You will need a larger deposit for a buyto-let mortgage

If you’re purchasing a home, it’s common to put down a minimum of 5–10% of the property’s value as a deposit.

However, for a buy-to-let mortgage, you’re likely to need a much larger deposit. Usually, you’ll need a minimum deposit of 20% and 40% if you want to access the best deals.

2. The lender will review your credit report

A mortgage lender will review your credit history as part of the application process. So, it’s worth looking at your credit report first.

Lenders will be assessing how likely you are to default on the mortgage. Missed payments, county court judgments, or bankruptcy could be red flags.

Negative factors on your credit report don’t automatically mean you can’t secure a buyto-let mortgage. However, you may need to approach a specialist lender, and they may offer you a mortgage deal with a higher interest rate.

3. The mortgage provider will also consider the potential rental yield

As well as your credit report, the lender will consider the potential rental yield of the property you want to purchase.

Unlike a residential mortgage, which is typically based on your income and outgoings, the amount you can borrow on a buy-to-let mortgage will usually be determined by the rental income the property generates.

Lenders calculate an interest cover ratio (ICR), which measures how much profit you’re likely to make against the mortgage repayments. Lenders will typically require the rental income to be at least 125% of the mortgage payments you’ll be committing to. However, some lenders may impose a higher ICR.

If you’re a “portfolio landlord”, often described as having more than four properties, it can be more difficult to secure additional finance. Lenders may use a different ICR when assessing your application.

Some lenders may also use a system of “top slicing”. This is where they may consider other income you receive, such as a salary or pension, to bridge a shortfall when reviewing your application. However, this is rare, so if it’s something you’d like to do, you should approach a mortgage broker.

4. Most buy-to-let mortgages are interest-only

When you take out a mortgage to purchase your own home, it will usually be a repayment mortgage. This means you’re making interest payments and are paying off a part of the loan each month.

In contrast, buy-to-let mortgages are usually interest-only.

As a result, you’ll just be paying off the interest that’s accumulated on the amount borrowed. So, your monthly repayments will be lower.

However, when you reach the end of the mortgage term, you will still owe the full amount that you borrowed, and it’s important to have a longterm plan. You may decide to take out another mortgage, sell the property, or make provisions so that you can pay off the loan.

5. The fees associated with a buy-to-let mortgage are typically higher

When taking out a buy-to-let mortgage, you should also budget for higher costs. The upfront costs of taking out a buy-to-let mortgage tend to be significantly higher than those of residential mortgages. It’s not uncommon for buy-to-let mortgage fees to be thousands of pounds.

Remember, that a lower interest rate may not be as attractive as it first seems if the fees are higher.

The charges may be a flat fee or a percentage of the amount you’re borrowing.

3 taxes you may need to consider as a landlord

If you’re letting out a property, you will need to consider tax from when you purchase the property right through to when you sell it. It’s important to understand what your tax liability will be and how it will affect your overall plans.

Here are three key taxes you need to consider if you want to purchase a buy-to-let.

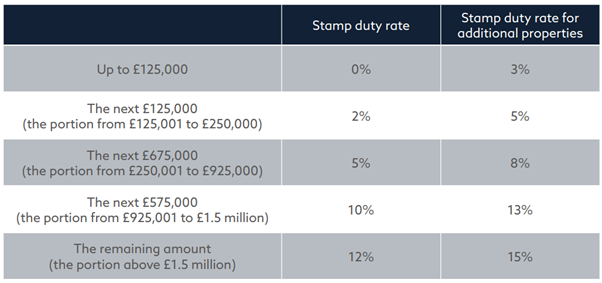

1. Stamp Duty

Stamp Duty is a type of tax that you pay when you purchase residential property or land in England and Northern Ireland.

The rate of Stamp Duty depends on the value of the property. There is a 3% surcharge if you’re purchasing additional properties, including properties you’ll rent out. So, the rate of Stamp Duty you pay could be higher than you expect.

The table below shows the Stamp Duty rates for the 2022/23 tax year.

You must pay Stamp Duty within 14 days from the completion date. As a result, it’s essential that you understand how much you will need to pay and include this in your budget when you’re purchasing a buy-to-let property.

There are similar types of tax in Scotland (Land and Buildings Transaction Tax) and Wales (Land Transaction Tax), both of which include a surcharge if you’re purchasing a buy-to-let property.

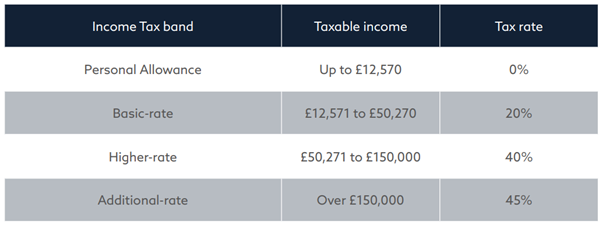

2. Income Tax

As a landlord, you’ll normally need to pay Income Tax on the rent you receive from your property.

In addition, you may need to pay Income Tax on other payments from tenants for services you may provide as a landlord, such as cleaning communal areas, utility bills, or arranging repairs to the property. Non-refundable deposits and any money that you keep from a refundable deposit at the end of a tenancy will also count as income.

The rate of Income Tax you pay will depend on your total income. So, you’ll need to consider things like your salary and pension when calculating how much tax you’ll be liable for. Keep in mind that rental income could push you into a higher tax bracket.

The below table shows the Income Tax thresholds in England, Wales, and Northern Ireland for the 2022/23 tax year.

There are allowances and deductions that could reduce the amount of Income Tax you will be liable for, which are covered later in this guide.

Income Tax bands are different in Scotland.

If your total income from UK property is £10,000 or more for the tax year (before expenses are deducted), you must complete a tax return. You will also need to do this if your rental income is more than £2,500 after deducting rental expenses.

If your income after deductions is under £2,500, HMRC may be able to collect the tax through the PAYE system if you’re paying tax this way, either through a salary or your pension.

3. Capital Gains Tax

Finally, you may be liable for Capital Gains Tax (CGT) if you sell the property in the future.

CGT is a type of tax that you pay when you sell some assets, including property that isn’t your main home, and make a profit.

For the 2022/23 tax year, you have a CGT allowance of £12,300. So, if the profit you make when selling assets falls below this threshold, you won’t need to pay CGT.

The rate of CGT you pay on profits above the allowance depends on your Income Tax band. However, for profit made on the sale of residential properties, it can be as high as 28%.

Understanding what CGT will be payable is crucial for calculating how much you’ll make when selling a buy-to-let property.

While CGT may not be something that will affect your plans now, it could affect your longterm goals and whether purchasing property is the right option for you.

You must keep records for at least five years after the 31 January tax return deadline for each tax year. HMRC can charge you a penalty if your records are not accurate, complete, and readable, or if you do not keep them for the required time period.

What can you do to reduce your tax liability?

Changes in recent years mean that allowances available to landlords aren’t as generous as they once were. For instance, landlords can no longer deduct mortgage interest from their income.

However, there are still steps you can take to reduce your tax liability.

As an individual, the first £1,000 of your income from property rental is tax-free. This is known as the “property allowance”.

You can also deduct some expenses from your rental income if you pay for them yourself when calculating your tax liability. This may include things like:

- General maintenance and repairs to the property, but not improvements

- Water rates, Council Tax, gas, and electricity

- Insurance, such as landlords’ policies for buildings, contents, and public liability

- Cost of services, such as the wages for gardeners or cleaners

- Letting agent fees and management fees

- Legal fees for lets of a year or less, or for renewing a lease for less than 50 years

- Accountant’s fees.

If you have more than one property, all rental receipts and expenses can be lumped together. So, expenses on one property can be deducted from receipts of another.

You can also deduct expenses that are “wholly and exclusively” for the purpose of renting out the property.

For example, if you purchase cleaning products specifically for cleaning the rental property before a new tenant moves in, you can deduct these expenses. However, you cannot deduct the cost of a new vacuum cleaner for your home, which you use to clean the rental property.

Depending on your circumstances there may be other things you can do to reduce your tax liability, such as setting up a limited company. If you’d like to discuss your options, please contact us.

How to find the right buy-to-let property to invest in

There are lots of things to consider if you want to purchase a buy-to-let, not least finding the right property.

Here are some of the things you should consider when you’re searching the property market.

1. Is the location desirable?

Everyone’s heard the property mantra “location, location, location!” and when it comes to buy to-let it’s something you should keep in mind.

Will the location of the property make it desirable to a tenant, and is there demand in the local market for rental properties?

In addition to whether the property is appealing to tenants, you should consider how it suits your needs and plans.

If you want to manage the property by yourself, is it close to your own home and accessible if you need to visit in an emergency? You don’t have to discount a property that is further away, but you may want to consider using a letting agent to manage it.

2. What are your ideal tenants looking for?

It’s a good idea to have an ideal tenant in mind, and consider who will be looking for a rental property in the area you’re buying.

A home a young professional will be looking for will be very different to what a family of five needs. Understanding the market and who lives in the area can mean you’re able to focus on the properties that are more likely to attract tenants.

If you’re in an area with lots of young professionals, flats in the heart of a city centre or with excellent transport links could be right. While if you’re focusing on families, extra bedrooms, outdoor spaces, and good schools are likely to be priorities.

According to Aldermore, these are the 10 best towns and cities for a buy-to-let investment.

- Bristol

- Oxford

- Cambridge

- Manchester

- Luton

- London

- Northampton

- Brighton

- Reading

- 10. Norwich

3. What maintenance will be required?

The money you need to spend on maintaining and repairing a property will eat into your profits. So, it’s something you should think about from the outset.

Don’t just consider the things that will need doing immediately. If you’re investing in a buy-to-let for the long term, what work is likely to need completing in the next 10 years? The roof may be in good order now, but if it needs replacing in a few years it could cost you thousands of pounds.

That doesn’t mean you shouldn’t invest in properties that need work. You may be able to find a property with a lower purchase price if you’re willing to invest in it, but make sure maintenance costs are part of your budget.

4. What is the potential yield of the property?

When you’re investing in a property, reviewing the potential return is crucial. Will the property provide you with your goal income?

Take some time to review what other properties nearby are rented out for and speak to local estate agents to get a realistic figure.

As mentioned previously, the rental yield is also used when assessing your application for a mortgage. You will often need a rental yield that is at least 125% of your mortgage repayments. So, if your mortgage repayments are £1,000 a month, the rental income generated by the property will normally need to be £1,250 a month.

5. Is the property energy-efficient?

How energy-efficient a property is might not be high on your list of things to consider when you’re looking at the options. However, a government proposal means it’s essential that you do.

All properties that are being sold or rented are required to have a valid Energy Performance Certificate (EPC). An EPC shows how energyefficient a home is and gives it a rating from A to G.

A new proposal would mean that all new lets will need a minimum EPC rating of C by 2025, and by 2028 for existing lets.

If you purchase an inefficient property, it could mean you need to spend significant sums to improve the EPC rating if the government introduces the new rules.

According to data from real estate agents Hamptons, half of all homes purchased by investors in the first quarter of 2022 have an EPC rating of C or above. The most efficient homes are usually new-builds.

There are also other reasons to choose an energy-efficient property. It can make your buy-to-let more attractive to potential tenants, who would benefit from lower energy bills. A growing number of banks and building societies will also offer a lower interest rate for energyefficient properties.

Do you have questions about buy-to-let mortgages or taxes for landlords?

If you have questions about how a buy-to-let mortgage will work and what option is right for you, or you want support to reduce your tax liability, please contact us. We’ll help you have confidence in the decisions you make.

If you’re thinking about becoming a landlord, we can help.