How has inflation affected the cost of living in the UK?

Inflation is taxation without legislation.

– Milton Friedman, American economist, statistician, and recipient of the 1976 Nobel Prize in Economic Sciences

As economies gradually return to normal following Covid-19 restrictions, inflation has begun to rise. It’s not only been featured on the news, but you may have also noticed when doing your shopping or paying your bills that prices are slowly creeping up.

In simple terms, inflation means the cost of goods rise. The higher the rate of inflation, the quicker prices are rising. Rising costs, especially when it’s at a rate higher than expected, can place families and businesses under financial pressure. In fact, according to a poll from interactive investor, more than a fifth of people say the rising cost of living is the biggest threat to their personal finances in 2022.

Understanding inflation and how it affects your wealth is crucial for creating an effective budget. It can also help you understand how the value of your assets will change over the long term. As inflation isn’t something you have control over, it can be difficult to calculate the effect it can have on your plans. Read on to find out more about inflation and what it could mean for you.

How is Inflation Calculated?

In the UK, the Office for National Statistics (ONS) is responsible for measuring inflation and reporting the findings, while the Bank of England (BoE) is responsible for keeping inflation stable.

The headline figures for inflation you see in the news are usually from the Consumer Price Index (CPI). To calculate this, the ONS looks at 180,000 prices for around 700 different items that it puts into a “shopping basket” of goods. The items in the shopping basket change depending on shopping habits and range from food to transport. Back in 1940, women’s corsets and condensed milk were staples included, whereas in 2021, hand sanitiser and smartwatches were added.

The average cost of the goods in the basket is then compared with the cost of the previous year to deliver an inflation rate.

Using the CPI, in the 12 months to March 2022, the rate of inflation was 7% – the highest rate for 30 years.

While CPI can give you a useful snapshot of how the cost of living has changed, it does have limitations. For a start, it only measures items that are in the basket. The data can also be skewed if one area of spending has seen prices rise rapidly

There are other ways of calculating inflation too. The Retail Price Index (RPI) is similar to the CPI but also includes mortgage interest payments, so it’s influenced by house prices and interest rates. As a result, the RPI in February 2022 was higher than the CPI at 9% as it reflected climbing property prices.

Confusingly, the UK uses both the CPI and RPI when calculating price increases. So, while your State Pension may increase by inflation as measured by CPI under the triple lock, an index-linked annuity purchased in retirement may be linked to RPI.

Is inflation good or bad?

A bit of inflation can be a good thing for the economy. It can encourage people to spend now as they expect prices to rise in the future. This, in turn, means businesses have the money to invest.

However, too much inflation can have the opposite effect. Rather than encouraging people to spend more, people may choose to delay spending either because they think they’ll get a better deal by waiting or because they’re worried about other costs increasing.

Maintaining the “right” level of inflation is the responsibility of the BoE. The Bank has a target to keep inflation around 2%. This is designed to stimulate the economy without encouraging people to hoard money.

Why high inflation is linked to rising interest rates

When inflation is high, one of the things the BoE can do is raise interest rates. Higher interest rates mean the cost of borrowing rises, so consumers and businesses have less money to spend. As a result, it can help to slow down inflation.

The BoE took this step in March 2022 and increased its interest base rate from 0.5% to 0.75%.

3 other “-flations” that could affect economies and wealth

Inflation is covered a lot in the news, but there are other “-flations” in finance that can affect economies and wealth.

Deflation: This is the opposite of inflation, and occurs when the price of goods and services fall. It typically signals that there is high supply but low demand.

Hyperinflation: Hyperinflation refers to a period of extreme inflation, typically when prices have increased by more than 50% in a month.

Stagflation: When the economy is experiencing slow growth and high levels of unemployment at the same time, it is known as “stagflation”.

HOW HAS INFLATION AFFECTED THE COST OF LIVING IN THE UK?

The arithmetic makes it plain that inflation is a far more devastating tax than anything that has been enacted by our legislatures. The inflation tax has a fantastic ability to simply consume capital.

– Warren Buffett, American business magnate and investor

The UK has benefited from relatively stable rates of inflation for more than a decade. Even so, you will have noticed that the cost of living has increased.

Between 1989 and 2021, the annual average rate of inflation has been 3.1%. The average annual increase can seem insignificant when you look at it in isolation, but inflation has a compounding effect. If you had an income of £1,000 a month in 1989, the Bank of England (BoE) calculates that you’d need an income of £2,645.30 a month today to meet the same standard of living.

Inflation will provide an idea of how your overall expenditure has changed or will change. However, there will be a large difference between different items included in the CPI measurement. Wider market conditions mean household energy bills increased at a much faster pace than the headline CPI figure in 2021, for example. So, you may notice some of your expenses rising due to inflation more than others.

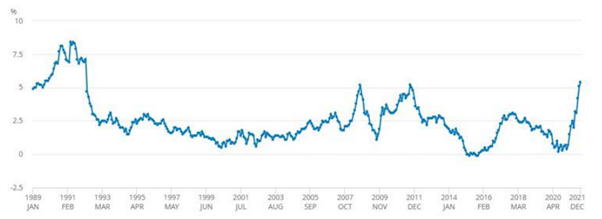

As the graph below demonstrates, the rate of inflation in the UK has varied a lot. There have been periods where the cost of living decreased, and others where it’s exceeded 8%.

Source: Office for National Statistics

Since 1989, the highest point of inflation was 8.4% in June 1991, but you may remember inflation being much higher in the 1970s and 1980s. An oil crisis led to inflation reaching 12.9% in March 1974, which led to many families struggling and unemployment rising.

Why is Inflation High Now?

While we haven’t reached record highs of inflation yet, the current figure is still well above the BoE’s target.

The BoE explains that there’s more than one reason why the rate of inflation started to rise in 2021, but a lot of it was to do with the economy recovering from the Covid-19 pandemic. As lockdown restrictions eased and the economy reopened, people began spending more money. However, lockdowns around the world had created supply shortages and challenges in shipping goods, and this block in the supply caused prices to rise.

The last few years have presented unique challenges to families, businesses and economies, and as the recovery continues the BoE expects the inflation rate to return to lower levels.

The Bank said: “We know some people are worried there will be a return to the high rates of inflation the UK experienced in the 1970s. But we are confident that inflation will not get anywhere near those levels this time.

“We expect inflation to stay high over the coming year, then start to fall back towards 2%.”

Rising Inflation Affects the cost of borrowing too

Inflation doesn’t just affect the cost of purchasing items or services – it also affects the cost of borrowing.

One of the things the BoE can do to control inflation is to increase interest rates. This is a step the Bank took in March 2022 when it increased the interest base rate from 0.5% to 0.75%. While a relatively small increase, and still far below historic levels of interest, the rise will affect millions of families.

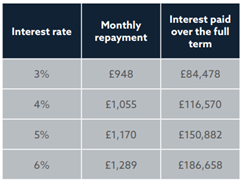

If you are repaying debt that doesn’t have a fixed interest rate, the amount of interest you pay is likely to rise as the BoE changes the base rate. For larger forms of debt, such as a mortgage, even a small change in the interest rate can have a huge impact on expenses and disposable income.

The table shows how even a relatively small increase in interest rates can affect the cost of a £200,000 repayment mortgage over a 25-year term.

Source: Money Saving Expert

So, as inflation and interest rates rise, families also need to consider how it will affect their borrowing and long-term plans.

21% of Britons think inflation will continue to exceed 5% in 2022

The BoE’s Inflation Attitudes Survey found that people are worried about the effects of inflation.

In November 2021, more than a fifth believed that inflation would exceed 5% over the next year, and 55% said if prices started to rise faster than they do now it would weaken Britain’s economy.

The survey found that 45% of people also expected rising inflation to lead to interest rates rising a little over the next 12 months, while 14% thought they would rise a lot.

The Retail Price Index:

How has your Grocery bill changed?

The Retail Price Index (RPI) measures how regular purchases have changed in value. From what you pick up at the supermarket to electronic goods, RPI is used to measure the rate of inflation in the UK.

When you look at how supermarket staples have changed in price, you might be surprised to see that some of the things you regularly put in your basket have changed little over the years, and in some cases, have even become cheaper.

Here are how some of your kitchen essentials have changed in price between January 1995 and December 2021.

Source: Office for National Statistics

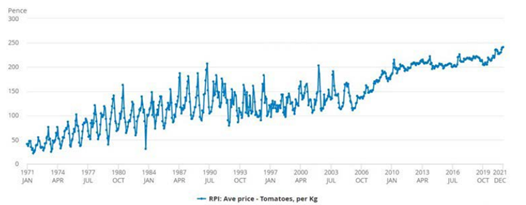

When you look at how inflation has affected the value of goods, you can see that grocery prices have become more stable, particularly for fresh produce. The graph below shows the price of 1kg of tomatoes. Throughout the 20th century, the price was affected by the seasons far more than the last two decades.

Source: Office for National Statistics

It’s not just the food and drink that you purchase in shops that are considered either; from restaurant meals to a drink in the pub, your spending in a variety of places is affected by inflation.

In February 1987, if you wanted a pint of draught lager, you’d expect to pay around £0.92. It’s been many years since a pint was less than £1 and in December 2021, a pint would set you back by around £4.02. That’s a price increase of more than 336%.

As well as food and drink, measuring inflation considers everything from electricity to packaged holidays.

QUIZ

How much does it cost?

While you’ve probably noticed your grocery shopping has crept up over the years, can you remember how much items used to cost?

- In 2021, a pint of milk would set you back £0.46. What did it cost in 1990?

- A white loaf of sliced bread cost £1.07 in 2021. What was the average price in 2013?

- A 250g butter block cost £1.78 in 2021. What did it cost in 2016?

- In 1992, how much would you pay for 1kg of best beef mince? In 2021, it was £6.39.

- 1kg of chicken to roast cost £2.78 in 2021. What was the price in 2007?

- How much would 1kg of Cheddar cheese cost you in 1997? Today, it would cost around £6.21.

- Iceberg lettuce cost £0.52 in 2021, but how much was it at the end of 2004?

- If you purchased a kilogram of bananas in 2021, it would cost £0.81. What would it cost in 1995?

- 100g of pure, instant coffee cost £3.02 in 2021. How much was the same item in 1992?

- How much would you pay for 250g of tea bags in 1986? In 2021, it would set you back £2.05.

Source: Office for National Statistics

When Inflation Surges:

3 Case Studies from around the world

Inflation isn’t anything new and there is a range of factors that can cause the cost of living to rise at a faster pace than expected. These three case studies highlight the impact hyperinflation can have on the value of money, families, and economies around the world.

Germany, 1923

Germany’s period of hyperinflation followed the first world war and was partly due to the government funding war operations through borrowing. Coupled with the expensive war reparations demanded by the Treaty of Versailles, Germany experienced hyperinflation for over a year.

During this period, prices doubled every 3.7 days, and the highest monthly rate of inflation was a huge 29,500% in October 1923. This hyperinflation led to Germany’s currency becoming almost worthless and at one point, 4.2 trillion German marks were worth just 1 American dollar. In scenes that may seem strange out of context, children played with massive piles of cash and families used banknotes for fuel as it was cheaper than the alternatives.

While the currency and economy eventually stabilised, the economic pressure it led to is often viewed as playing a role in the rise of the Nazi party.

Zimbabwe, 2008

A more recent example of hyperinflation occurred in Zimbabwe in 2008. While the government stopped reporting official inflation rates during the worst months, it’s estimated that prices doubled almost every 24 hours, with November 2008 having a massive inflation rate of 79,600,000,000% (79.6 billion percent).

In a bid to get a handle on the hyperinflation, the government imposed a cap on bank withdrawals and introduced a $100 million banknote, which led to prices soaring even further. Reportedly, a loaf of bread rose from $2 million to $35 million overnight.

Zimbabwe’s hyperinflation goes back to 1980 when the country adopted a new currency as it gained its independence. Lapses in government policy and severe shortages of essential goods, including food, contributed to inflation soaring. Eventually, the Reserve Bank of Zimbabwe intervened and re-priced the currency.

Hungary, 1946

The worst case of hyperinflation recorded was in Hungary in 1946. When the second world war started, Hungary was already in a weak economic position and the central bank, which was under the government’s control, printed money to meet the government’s budget needs without financial restraint.

At the height of Hungary’s hyperinflation, it’s estimated that the daily inflation rate was 195%, meaning prices doubled every 15.6 hours. Over a month, that means prices were increasing by a staggering 13,600,000,000,000,000% (13.6 quadrillion percent). Before hyperinflation, the highest domination banknote was 1,000 pengo, in 1946 the highest denomination banknote was 100,000,000,000,000,000,000 (one hundred quintillion).

The pengo was eventually replaced in a currency revaluation in August 1946. To put into perspective the damage hyperinflation did, when the currency was replaced, the total of all Hungarian banknotes in circulation was estimated to be equal to just onethousandth of a US dollar.

The Economic Impact of Deflation

It’s not just periods of hyperinflation that can affect the economy – deflation can too. Perhaps one of the most well-known periods of deflation occurred during the economic depression of the 1930s, dubbed the “Great Depression”.

The depression started in the US in 1929 and lasted until 1933. On 29 October 1929, the stock market crashed on a day that’s become known as “Black Tuesday”, when investors traded some 16 million shares on the New York Stock Exchange in a single day. Between 1929 and 1932, it’s estimated that worldwide GDP fell by 15%. This compares to a fall of less than 1% during the 2008/09 financial recession.

In the US, prices fell an average of 10% a year between 1930 and 1933, and coupled with a dramatic drop in output, it had a profound impact on the economy. Deflation affected prices and led to firms laying off workers and struggling to meet debt obligations. In turn, this affected household income and increased the chances of families defaulting on debts too, which led to banks failing. This created a vicious circle as the money stock contracted further and prices, employment and output all continued to decline.

Balancing Inflation

While the aforementioned case studies of deflation and hyperinflation are extreme examples, they do highlight why managing inflation is an essential part of the Bank of England’s (BoE) responsibilities. Too much inflation can lead to currency devaluing, too little can play a role in an economic recession.

The rate of inflation has a huge effect on the way people, businesses, and governments spend or use their money. The BoE’s 2% inflation target aims to keep the UK’s inflation low and stable.

Have your Assets and Income and kept pace with inflation?

If the value of your assets doesn’t rise at the same pace as inflation, they are losing value in real terms.

How the value of your assets has changed over time will depend on a plethora of things, but the data below can give you an idea of how your assets and income may have increased or decreased in value over time.

Savings Vs Inflation

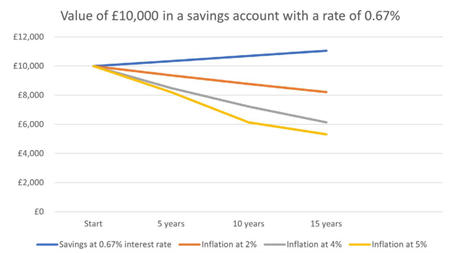

While money sitting in a savings account doesn’t change in value, other than some interest normally being added, its spending power can decrease. As the cost of goods and services rise, savings that aren’t earning enough interest to match or outpace inflation will gradually be able to buy less and less.

Royal London compared the growth of £10,000 held in a savings account over 5, 10, and 15 years, assuming an interest rate of 0.67%. The below graph highlights how different rates of inflation will reduce the value of your savings in real terms over time.

Source: Royal London

For more than a decade, interest rates have been below 1%, so savers have struggled to find savings accounts that ensure their money keeps pace with inflation. If you’ve held money in a savings account, when you consider the effects of inflation, the value has probably decreased in real terms.

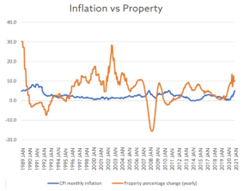

Property Vs Inflation

Property prices have been soaring in recent years. According to the Halifax House Price Index, the average property price in the UK hit a record high in March 2022 as it reached £282,753. For many people, their home is one of the largest assets they own. So, how have property prices fared against inflation?

The graph below shows the annual percentage change of property prices in the UK compared to the inflation rate. While there are some occasions where property prices have fallen sharply when compared to inflation, notably during the 1990s recession and following the 2008 financial crisis, property prices have largely outpaced inflation. If you’ve been a homeowner for several decades, it’s likely the value of your property has increased in real terms.

Source: Land Registry

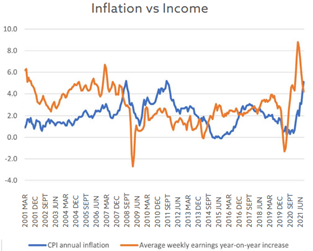

Wages Vs Inflation

Inflation doesn’t just affect how much the items you buy cost, but how far your income will go. If your income fails to keep up with inflation, you may have to adjust your budget and plans.

The graph below shows how average wage growth compares to inflation over the last 20 years. At times, wages have increased at a faster pace, so, on average, spending power will have increased, but there are times when your income may have been worth less in real terms.

Source: Office for National Statistics

The data highlights how economic factors affect wage growth. The two largest dips occur following the 2008 financial crisis and in 2020, when many workers received a lower income due to being furloughed during the Covid-19 pandemic, with a sharp rise following the pandemic restrictions being lifted.

For short-term saving goals, the effects of inflation on your savings will be minimal. But, if you’re planning to hold that money for a long period, annual inflation can quickly compound.

The graph below shows how average wage growth compares to inflation over the last 20 years. At times, wages have increased at a faster pace, so, on average, spending power will have increased, but there are times when your income may have been worth less in real terms.

If you deposited a lump sum of £40,000 into your savings account in 2010, it will have needed to grow by £14,573,08 just to provide you with the same spending power in 2021, according to the Bank of England. This is because inflation has averaged 2.9% annually

If your savings account has matched the pace of inflation, your savings will be worth the same in real terms, but in the current lowinterest-rate environment, it’s unlikely.

Interest rates have been at historic lows since the 2008 financial crisis to support the economy. In fact, the Bank’s base rate has not increased above 1% since 2009. As a result, it’s likely that any savings you have will have fallen in value in real terms for more than a decade.

When you consider how inflation can affect your savings, which you may have thought of as “safe”, it’s easy to see why an interactive investor poll found that people consider inflation the second biggest threat to their personal finances.

Why Inflation Could Mean the value of your savings is falling in real terms

Putting your money in a savings account is often seen as a safe way to preserve your wealth. After all, it’s there to access whenever you need it and the figure in the account isn’t going to decrease. Assuming you stay within the limits of the Financial Services Compensation Scheme, your money is protected even if a bank or building society fails.

However, once you factor in inflation, the value of your savings is probably falling in real terms. As the cost of living rises, the spending power of your savings has decreased. So, while your savings may remain the same, or grow modestly, you will be able to buy less with the money.

Does Investing Provide a Solution?

For some savers, investing could provide a way to ensure their wealth keeps pace with inflation or exceeds it.

Investing your money in stocks, shares, bonds, and other assets could deliver returns higher than the interest rate you receive on a savings account. This can help you maintain your spending power or even help to grow your wealth over the long term.

However, investing does expose your money to risk. All investments carry some level of risk and investment markets experience periods of volatility. For this reason, you should only invest if you have a time frame of at least five years. This provides an opportunity for the peaks and troughs to smooth out.

How long you will be investing plays a role in your risk profile, which evaluates what level of investment risk is appropriate for you. Your risk profile should also consider things like your investment goals, other assets you hold, and your attitude to risk. If you’d like to discuss your risk profile, please contact us.

Investment risk can be worrisome. While 22% of people said inflation was a fear in the interactive investor poll, 56% said a stock market crash was the biggest personal finance risk in 2022. Investment values can fall, and stock market crashes do happen, but looking at the long-term trend is important.

Thinking about investing? An ISA could be right for you

An ISA can provide a tax-efficient way to save or invest.

Returns from investments held in a Stocks and Shares ISA are free from Income Tax, Capital Gains Tax, and Dividend Tax. Choosing to invest through an ISA can reduce your tax bill and help your money go further.

For the 2022/23 tax year, you can place up to £20,000 into an ISA. This allowance can either be held in a Cash ISA, a Stocks and Shares ISA, or spread across both.

Historically, stock markets have recovered following a crash. The crash in 2020 caused by the Covid-19 pandemic highlights this. According to the Guardian, the FTSE 100, an index of the 100 largest companies listed on the London Stock Exchange, fell by 14.3% in 2020, its worst-performing year since the 2008 financial crisis. During those 12 months, investors experienced high levels of volatility.

Seeing investment values fall can lead to concern, yet the markets did recover relatively quickly. Those investors that held their nerve and didn’t sell during the volatility are likely to have benefited overall. In fact, in 2021, the FTSE 100 bounced bank to finish 14.3% up after its best year since 2016, a Guardian report finds.

If you are thinking about investing, it’s important to note that returns cannot be guaranteed and past performance is not a reliable indicator of future performance. You should take the time to assess your circumstances and how investing can fit into your financial plan.

Inflation and Retirement:

Could it erode your spending power?

While it can be easy to overlook the effects of inflation day-to-day, it can have a huge effect on your retirement lifestyle if you’ve not thought about it.

It’s not uncommon for retirement to span several decades. Over the years, inflation will add up and your retirement income won’t stretch as far. If you overlook inflation, it could mean you struggle financially in your later years or you’ll be unable to cover unexpected costs, such as needing some form of care.

The Bank of England’s inflation calculator demonstrates how inflation could reduce your spending power in retirement. Let’s say you retired in 2010 and began taking an income of £28,000 to live comfortably. The average annual rate of inflation over the next decade is 2.9%. So, to achieve the same standard of living in 2021, your income will need to have increased to £38,201.16.

Now imagine the effect inflation could have over a full retirement that is likely to be two or three times longer, especially if the rate of inflation is much higher. If you hadn’t planned to take a greater income in your later years or haven’t taken steps to increase your wealth, you risk running out of money or needing to cut back your plans.

According to research from abrdn, 1 in 3 retirees worry they won’t have enough money to last throughout retirement. Reviewing your finances at retirement and how your income needs will change over time can provide you with the peace of mind you need to enjoy the next chapter of your life.

How long will your retirement last?

The effects of inflation compound over time. So, it’s important to think about how long you will be retired for.

The current State Pension Age in the UK is 66. Assuming you retire at this age, a man has an average life-expectancy of 85, so would spend almost two decades in retirement. For a 66-year-old woman, the average life-expectancy is 87.

While these figures can give you a rough idea of how long retirement can be, keep in mind that many retirees will live beyond the average age. For instance, a woman aged 66 has a 1 in 4 chance of celebrating her 94th birthday.

So, when calculating the effects of inflation on your retirement income, you need to think in decades rather than years. Source: Office for National Statistics

Source: Office for National Statistics

2 Ways you Could Protect your retirement income from inflation

As you retire, considering how to make sure your income keeps up with inflation can safeguard your future. Among the options to consider are the following two:

Purchase an annuity that’s linked to inflation

An annuity is something you can purchase which will then provide an income for the rest of your life. It’s an option that can provide financial security throughout retirement.

You can choose to purchase an annuity that will deliver an income that increases each tax year in line with inflation. This option will usually mean the annuity rate you’re offered is less, but, as it rises with inflation, it will maintain your spending power.

If you’re planning retirement with a partner, you may also choose a joint annuity that will provide an income for your loved one if you pass away (again, this may be linked to inflation).

Leave some of your pension invested

An alternative to purchasing an annuity is flexi-access drawdown. With this option, you can withdraw a flexible income from your pension to suit your needs, while the rest will typically remain invested.

As the money is invested, it has an opportunity to grow throughout your retirement and help your savings keep pace with inflation. However, investment returns cannot be guaranteed, and you will be responsible for ensuring your pension continues to provide an income for the rest of your life.

Depending on your circumstances and assets, there may be other options for you. Keeping the long-term effects of inflation in mind when you retire can help you create a robust plan that’s right for you.

Building a long-term financial plan that considers the effects of inflation

Inflation can affect your day-to-day outgoings and there’s a danger that it can affect your long-term plans and financial security too. As a result, it’s essential that inflation is considered when you’re setting your financial goals and creating a plan that you can have confidence in.

If you’re worried about the effect inflation could have on your plans, or want to speak to a professional about the steps you can take, please contact us.