Back in March, as the extent of the Covid-19 pandemic became known, Chancellor Rishi Sunak announced the government’s Job Retention Scheme.

Better known as the ‘furlough scheme’, it has helped nearly ten million people keep their jobs while continuing to earn 80% of their usual income and making their National Insurance and pension contributions.

At a cost of approximately £14 billion a month, the government has provided millions of workers with welcome financial stability during an otherwise unstable time.

But, if you have been furloughed, how has receiving only 80% of your normal pay affected your financial plan?

Your mortgage could be affected

With your household income reduced by 20%, continuing to make your mortgage payments might have been tricky. You may have taken advantage of a three-month mortgage payment holiday. According to This Is Money, 1.8 million people in the UK have taken advantage of a break from their payments.

While a break from payments may have offered you respite, remember that you will still need to repay the money later. This will most likely be in the form of higher monthly payments for the rest of the term of your loan.

The Guardian reports that a £200,000 mortgage taken out in May 2018 at a 2.5% rate costs £897 a month. If you take a three-month payment holiday, the cost will rise to £910 a month.

Credit reference agencies have confirmed that taking a mortgage payment holiday won’t affect your credit file. However, you should also be mindful that a mortgage holiday might affect your ability to borrow money in the future.

This is because lenders may look at other factors such as your bank account information when making decisions on loan applications. Taking a mortgage payment holiday, or extending your holiday, could indicate to a lender that your personal finances are stretched, and may, therefore, impact their decision to lend to you.

The news is more positive if you are on a tracker or variable rate mortgage. In March, the Bank of England cut the Base rate to 0.1%, meaning the rate of the interest you pay should have fallen. Lower mortgage payments could have left you with additional income to supplement what you lost during furlough.

Your pension contributions may have reduced

You might also be concerned about the effects of furlough on your pension. Although your pension contributions may not have stopped while you were furloughed, they could have been lower than usual.

As well as paying 80% of your salary up to £2,500 a month, the furlough scheme also replaced the 3% employer contribution into your pension pot on earnings between £520 and £2,500 a month. Note that this doesn’t include commission, fees, or bonuses, so any contributions made would have been calculated from your basic salary.

While your pension contributions may have continued, they would probably have been lower than normal. This is because they were based on just 80% of your salary. If you earn more than £30,000 a year, the £2,500 per month cap means your pension contributions could have fallen significantly.

Alternatively, you may have decided to reduce or suspend your contributions. If you have, or you are considering this, remember that this could have a significant impact on the value of your pension savings when you come to retire.

Remember to consider opting back in when you can afford it. Thanks to tax relief and employer contributions, pensions are a tax-efficient way to prepare for your retirement, and you may not want to lose out on these benefits in the long-term.

You could make hasty investment decisions

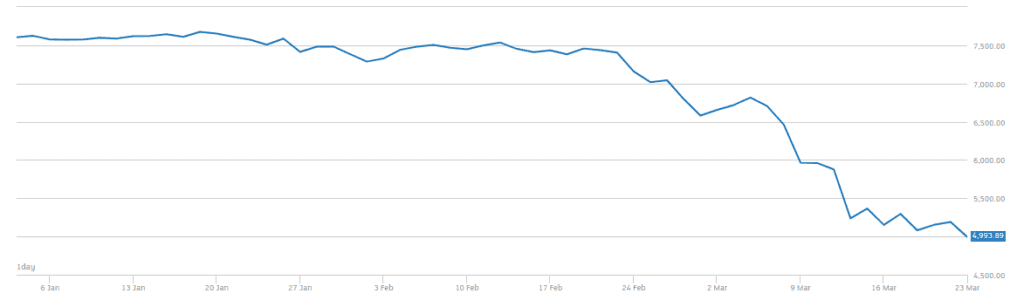

The pandemic has caused massive stock market volatility. In the UK, the FTSE 100 index lost around 34% of its value between 1st January and 23rd March 2020.

While many markets have recovered some of these losses, headlines concerning stock market volatility may have affected your confidence in your investments. You may be thinking about selling some of your assets or moving your funds to lower-risk investments to avoid further losses.

This may not be the best course of action. During short-term uncertainties, making emotional knee-jerk decisions about your investments can damage your long-term plans.

It’s worth remembering two things:

- You are likely to have a diversified portfolio. The fall in the value of stock markets is typically not the same as the fall in the value of your portfolio. Our clients have diverse portfolios that include exposure to other asset classes, for precisely this type of situation.

- It’s a bad time to panic. If your house had fallen in value in the short-term, it is unlikely that you would immediately put it up for sale and realise a loss. While our emotions might take over at this time, reacting to a fall in the markets can be a mistake, and many studies have found that this is one of the main reasons why investors lose money.

Stock markets are likely to remain volatile for some time. Fears of a second coronavirus wave, and continued economic uncertainty, mean that no one is quite sure how markets will play out in the coming months.

The key is patience. Over more than 100 years, markets have fallen and recovered and, in the long term, tend to generate positive returns. Your financial plan is designed to withstand turmoil in markets, and this current crisis is no exception.

You might be worried about redundancy

In recent months, you might have made significant changes to your financial arrangements. As the furlough scheme begins to wind down, you might need to make more.

Although designed to avoid job losses, the furlough scheme itself imposes no restrictions on employers making staff redundant. As companies reopen into a post-lockdown market, poor or unsustainable trading conditions could make redundancies unavoidable.

In July, the BBC reported that the end of the furlough scheme could lead to 1.2 million Britons being unemployed by Christmas.

Also in July, the government introduced laws to ensure that furloughed workers who lose their jobs will receive redundancy pay based on their normal wage, rather than their 80% furloughed income. However, the financial implications of redundancy could still be severe.

However Covid-19 has affected your finances, we can help

The job of a financial planner is to help you achieve your long-term financial goals. By getting to know your personal circumstances, your financial position, and your aspirations for the future, we can build a plan to help make your goals a reality.

An important part of the plan we make for you will be ensuring you are financially prepared for the unexpected. Many life events can bring financial uncertainty, but a well-constructed plan based on your individual circumstances will help protect you against financial shocks.

Balancing your needs in the short-term with your longer-term aspirations is a tricky juggling act, but it’s one we can help you with.

Get in touch

If you have any questions about your long-term financial plans or the potential impact of the furlough scheme on your goals and aspirations, please contact us. Email enquiries@futureplanningwm.co.uk or call 01793 575553.